The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Cumulus Media Inc. (NASDAQ:CMLS) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Cumulus Media Carry?

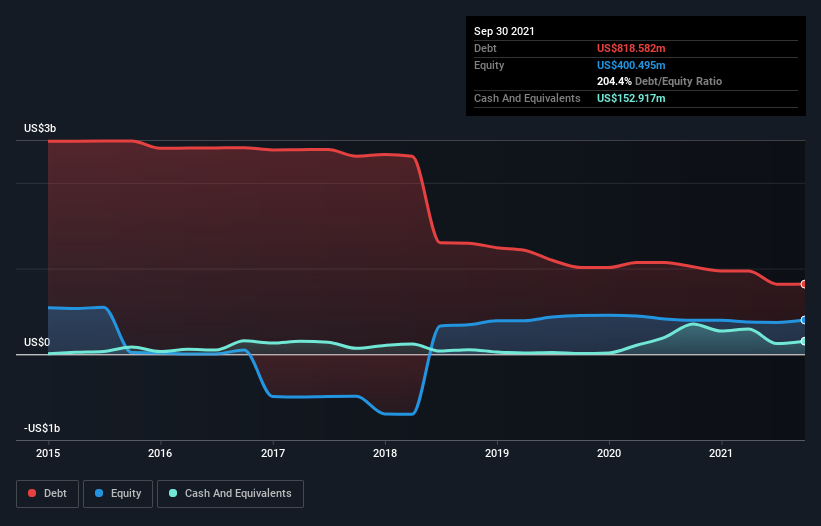

You can click the graphic below for the historical numbers, but it shows that Cumulus Media had US$818.6m of debt in September 2021, down from US$1.02b, one year before. However, it does have US$152.9m in cash offsetting this, leading to net debt of about US$665.7m.

How Healthy Is Cumulus Media’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Cumulus Media had liabilities of US$136.9m due within 12 months and liabilities of US$1.19b due beyond that. Offsetting these obligations, it had cash of US$152.9m as well as receivables valued at US$203.2m due within 12 months. So it has liabilities totalling US$965.8m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$228.2m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, Cumulus Media would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 0.89 times and a disturbingly high net debt to EBITDA ratio of 5.7 hit our confidence in Cumulus Media like a one-two punch to the gut. The debt burden here is substantial. The good news is that Cumulus Media grew its EBIT a smooth 99% over the last twelve months. Like a mother’s loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Cumulus Media can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Cumulus Media recorded free cash flow of 44% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

To be frank both Cumulus Media’s interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Overall, we think it’s fair to say that Cumulus Media has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt.