The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Adobe Inc. (NASDAQ:ADBE) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Adobe’s Net Debt?

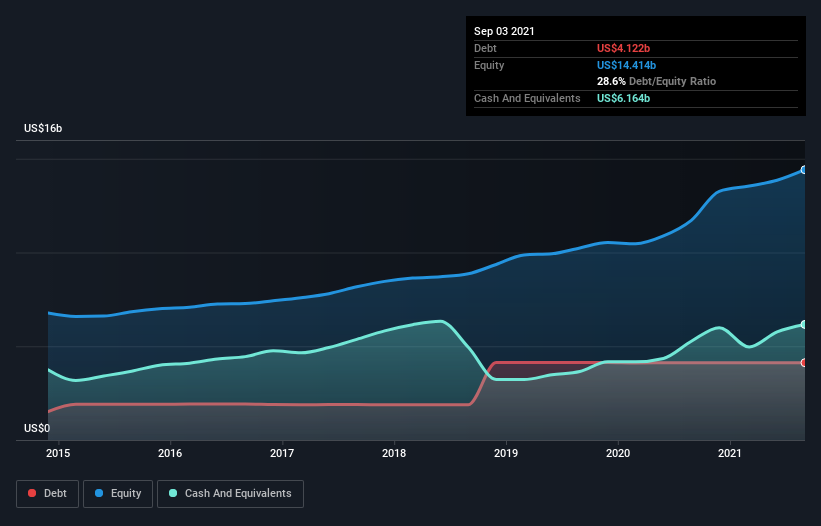

The chart below, which you can click on for greater detail, shows that Adobe had US$4.12b in debt in September 2021; about the same as the year before. But on the other hand it also has US$6.16b in cash, leading to a US$2.04b net cash position.

How Strong Is Adobe’s Balance Sheet?

The latest balance sheet data shows that Adobe had liabilities of US$6.19b due within a year, and liabilities of US$5.54b falling due after that. Offsetting this, it had US$6.16b in cash and US$1.55b in receivables that were due within 12 months. So it has liabilities totalling US$4.02b more than its cash and near-term receivables, combined.

Having regard to Adobe’s size, it seems that its liquid assets are well balanced with its total liabilities. So it’s very unlikely that the US$287.6b company is short on cash, but still worth keeping an eye on the balance sheet. Despite its noteworthy liabilities, Adobe boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that Adobe has boosted its EBIT by 38%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Adobe can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Adobe may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Adobe actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

We could understand if investors are concerned about Adobe’s liabilities, but we can be reassured by the fact it has has net cash of US$2.04b. The cherry on top was that in converted 122% of that EBIT to free cash flow, bringing in US$6.6b. So we don’t think Adobe’s use of debt is risky.