David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Verint Systems Inc. (NASDAQ:VRNT) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

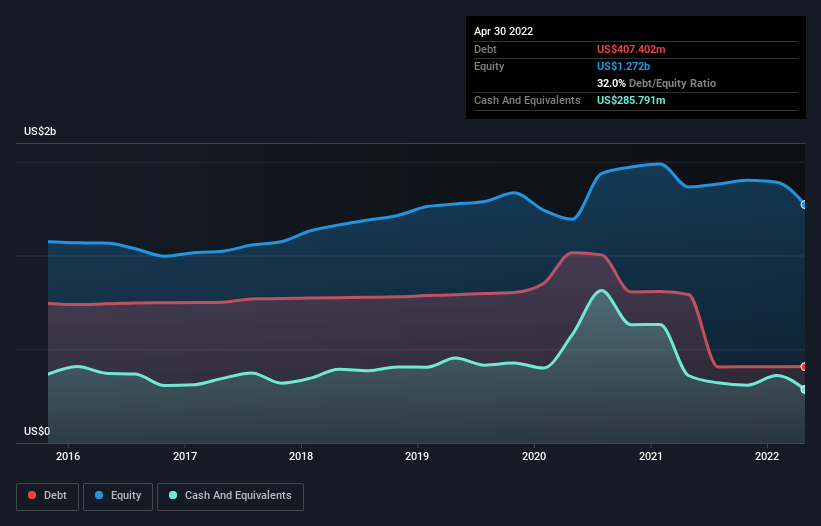

What Is Verint Systems’s Net Debt?

As you can see below, Verint Systems had US$407.4m of debt at April 2022, down from US$792.5m a year prior. However, because it has a cash reserve of US$285.8m, its net debt is less, at about US$121.6m.

How Healthy Is Verint Systems’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Verint Systems had liabilities of US$439.9m due within 12 months and liabilities of US$489.4m due beyond that. On the other hand, it had cash of US$285.8m and US$187.8m worth of receivables due within a year. So its liabilities total US$455.7m more than the combination of its cash and short-term receivables.

Since publicly traded Verint Systems shares are worth a total of US$3.02b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 1.1 times EBITDA, Verint Systems is arguably pretty conservatively geared. And it boasts interest cover of 9.9 times, which is more than adequate. On the other hand, Verint Systems saw its EBIT drop by 8.1% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Verint Systems’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Verint Systems actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

The good news is that Verint Systems’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its EBIT growth rate. Taking all this data into account, it seems to us that Verint Systems takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start.