Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies United Natural Foods, Inc. (NYSE:UNFI) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does United Natural Foods Carry?

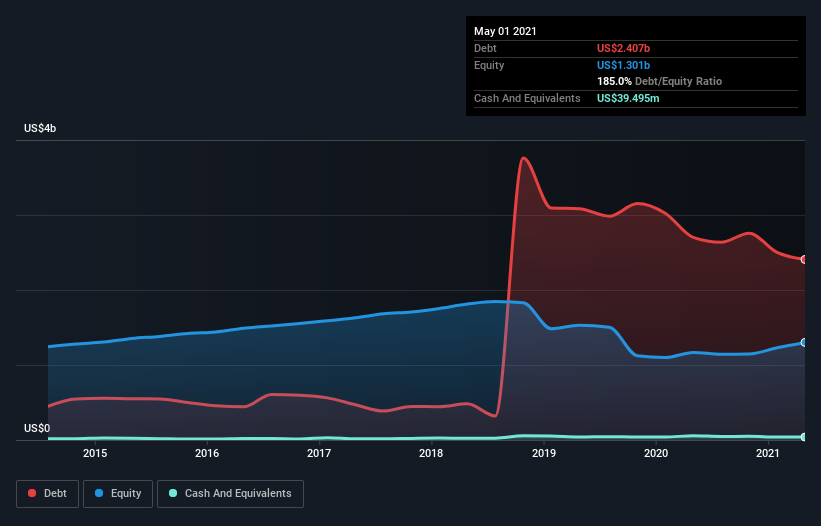

You can click the graphic below for the historical numbers, but it shows that United Natural Foods had US$2.41b of debt in May 2021, down from US$2.70b, one year before. And it doesn’t have much cash, so its net debt is about the same.

A Look At United Natural Foods’ Liabilities

According to the last reported balance sheet, United Natural Foods had liabilities of US$2.26b due within 12 months, and liabilities of US$3.95b due beyond 12 months. Offsetting this, it had US$39.5m in cash and US$1.12b in receivables that were due within 12 months. So its liabilities total US$5.06b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$2.07b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, United Natural Foods would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

United Natural Foods has a debt to EBITDA ratio of 3.2 and its EBIT covered its interest expense 2.5 times. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. On a slightly more positive note, United Natural Foods grew its EBIT at 17% over the last year, further increasing its ability to manage debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if United Natural Foods can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, United Natural Foods recorded free cash flow worth 60% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Mulling over United Natural Foods’s attempt at staying on top of its total liabilities, we’re certainly not enthusiastic. But at least it’s pretty decent at growing its EBIT; that’s encouraging. Once we consider all the factors above, together, it seems to us that United Natural Foods’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.