Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Tandem Diabetes Care, Inc. (NASDAQ:TNDM) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Tandem Diabetes Care’s Net Debt?

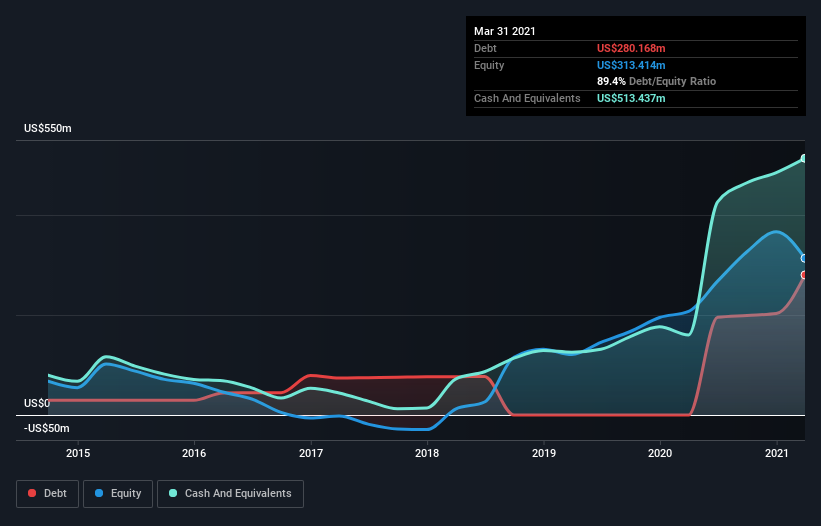

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Tandem Diabetes Care had US$280.2m of debt, an increase on none, over one year. However, its balance sheet shows it holds US$513.4m in cash, so it actually has US$233.3m net cash.

How Strong Is Tandem Diabetes Care’s Balance Sheet?

The latest balance sheet data shows that Tandem Diabetes Care had liabilities of US$103.4m due within a year, and liabilities of US$337.4m falling due after that. On the other hand, it had cash of US$513.4m and US$73.7m worth of receivables due within a year. So it actually has US$146.3m more liquid assets than total liabilities.

This surplus suggests that Tandem Diabetes Care has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Tandem Diabetes Care boasts net cash, so it’s fair to say it does not have a heavy debt load!

We also note that Tandem Diabetes Care improved its EBIT from a last year’s loss to a positive US$2.4m. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Tandem Diabetes Care can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Tandem Diabetes Care has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Tandem Diabetes Care actually produced more free cash flow than EBIT over the last year. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Tandem Diabetes Care has net cash of US$233.3m, as well as more liquid assets than liabilities. The cherry on top was that in converted 1,889% of that EBIT to free cash flow, bringing in US$45m. So we are not troubled with Tandem Diabetes Care’s debt use. The balance sheet is clearly the area to focus on when you are analysing debt.