Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that SilverBow Resources, Inc. (NYSE:SBOW) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

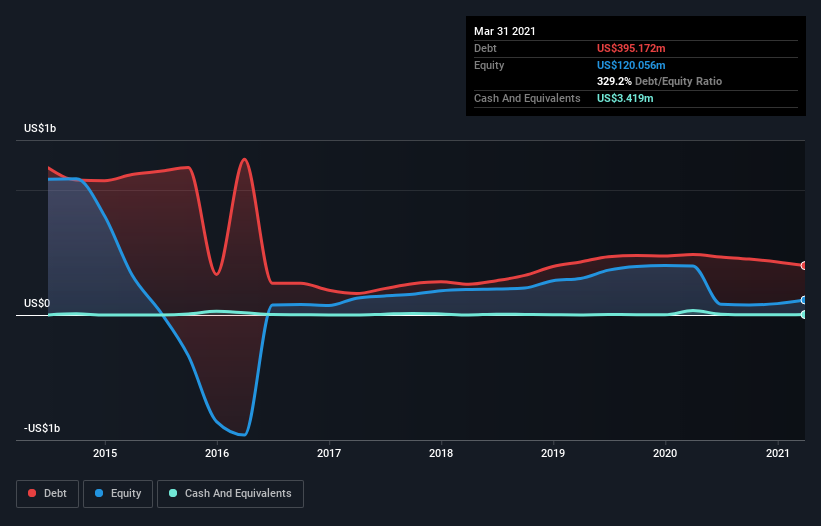

What Is SilverBow Resources’s Debt?

As you can see below, SilverBow Resources had US$395.2m of debt at March 2021, down from US$484.1m a year prior. And it doesn’t have much cash, so its net debt is about the same.

How Healthy Is SilverBow Resources’ Balance Sheet?

According to the last reported balance sheet, SilverBow Resources had liabilities of US$75.2m due within 12 months, and liabilities of US$405.2m due beyond 12 months. Offsetting this, it had US$3.42m in cash and US$26.1m in receivables that were due within 12 months. So it has liabilities totalling US$450.9m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$233.7m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, SilverBow Resources would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn’t worry about SilverBow Resources’s net debt to EBITDA ratio of 4.3, we think its super-low interest cover of 1.3 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even worse, SilverBow Resources saw its EBIT tank 82% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine SilverBow Resources’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, SilverBow Resources burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, SilverBow Resources’s EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. And furthermore, its interest cover also fails to instill confidence. Considering everything we’ve mentioned above, it’s fair to say that SilverBow Resources is carrying heavy debt load. If you harvest honey without a bee suit, you risk getting stung, so we’d probably stay away from this particular stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.