The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Repligen Corporation (NASDAQ:RGEN) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Repligen Carry?

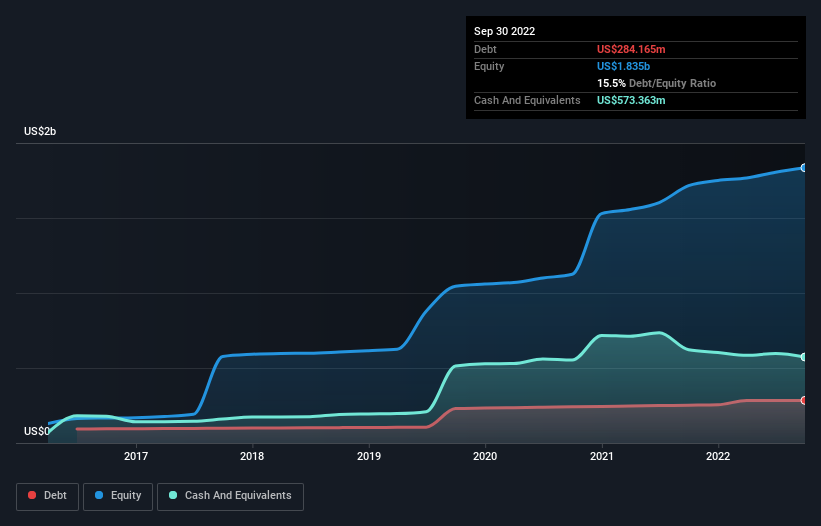

The image below, which you can click on for greater detail, shows that at September 2022 Repligen had debt of US$284.2m, up from US$252.3m in one year. But on the other hand it also has US$573.4m in cash, leading to a US$289.2m net cash position.

A Look At Repligen’s Liabilities

Zooming in on the latest balance sheet data, we can see that Repligen had liabilities of US$410.7m due within 12 months and liabilities of US$216.7m due beyond that. On the other hand, it had cash of US$573.4m and US$117.6m worth of receivables due within a year. So it actually has US$63.6m more liquid assets than total liabilities.

This state of affairs indicates that Repligen’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$8.82b company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that Repligen has more cash than debt is arguably a good indication that it can manage its debt safely.

In addition to that, we’re happy to report that Repligen has boosted its EBIT by 40%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Repligen’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. Repligen may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Repligen’s free cash flow amounted to 22% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing Up

While it is always sensible to investigate a company’s debt, in this case Repligen has US$289.2m in net cash and a decent-looking balance sheet. And we liked the look of last year’s 40% year-on-year EBIT growth.