Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Norfolk Southern Corporation (NYSE:NSC) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Norfolk Southern’s Debt?

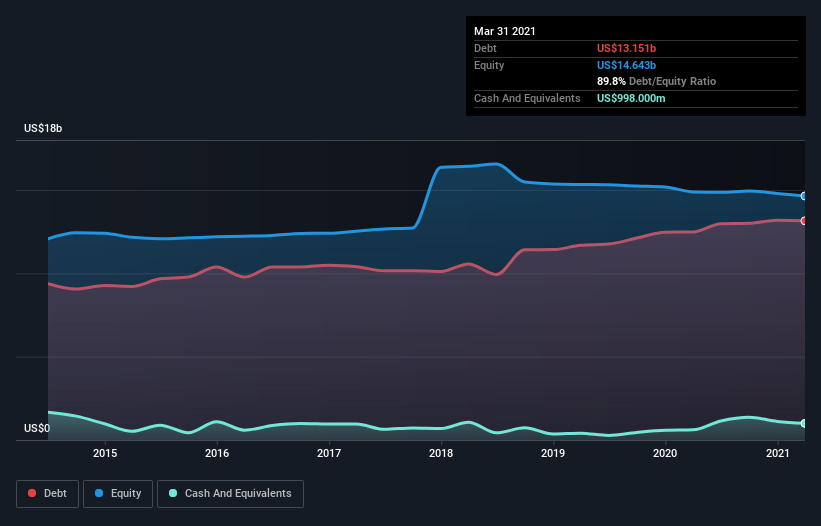

The chart below, which you can click on for greater detail, shows that Norfolk Southern had US$12.7b in debt in March 2021; about the same as the year before. However, because it has a cash reserve of US$998.0m, its net debt is less, at about US$11.7b.

How Strong Is Norfolk Southern’s Balance Sheet?

According to the last reported balance sheet, Norfolk Southern had liabilities of US$2.25b due within 12 months, and liabilities of US$21.0b due beyond 12 months. Offsetting this, it had US$998.0m in cash and US$944.0m in receivables that were due within 12 months. So it has liabilities totalling US$21.4b more than its cash and near-term receivables, combined.

Norfolk Southern has a very large market capitalization of US$71.5b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Norfolk Southern has net debt worth 2.5 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.7 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. The bad news is that Norfolk Southern saw its EBIT decline by 12% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Norfolk Southern’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Norfolk Southern recorded free cash flow worth 52% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Norfolk Southern’s EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example, its conversion of EBIT to free cash flow is relatively strong. Looking at all the angles mentioned above, it does seem to us that Norfolk Southern is a somewhat risky investment as a result of its debt. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.