Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that MicroStrategy Incorporated (NASDAQ:MSTR) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does MicroStrategy Carry?

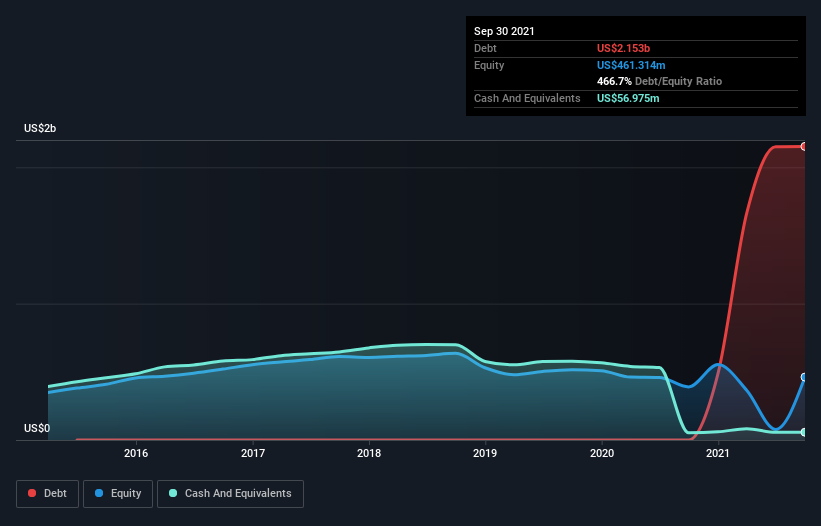

The image below, which you can click on for greater detail, shows that at September 2021 MicroStrategy had debt of US$2.15b, up from none in one year. However, it does have US$57.0m in cash offsetting this, leading to net debt of about US$2.10b.

How Healthy Is MicroStrategy’s Balance Sheet?

According to the last reported balance sheet, MicroStrategy had liabilities of US$253.9m due within 12 months, and liabilities of US$2.27b due beyond 12 months. Offsetting these obligations, it had cash of US$57.0m as well as receivables valued at US$124.9m due within 12 months. So its liabilities total US$2.34b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since MicroStrategy has a market capitalization of US$5.39b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

MicroStrategy has a rather high debt to EBITDA ratio of 27.4 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 3.3 times, suggesting it can responsibly service its obligations. The good news is that MicroStrategy grew its EBIT a smooth 60% over the last twelve months. Like a mother’s loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if MicroStrategy can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, MicroStrategy saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Neither MicroStrategy’s ability to convert EBIT to free cash flow nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But the good news is it seems to be able to grow its EBIT with ease. When we consider all the factors discussed, it seems to us that MicroStrategy is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.