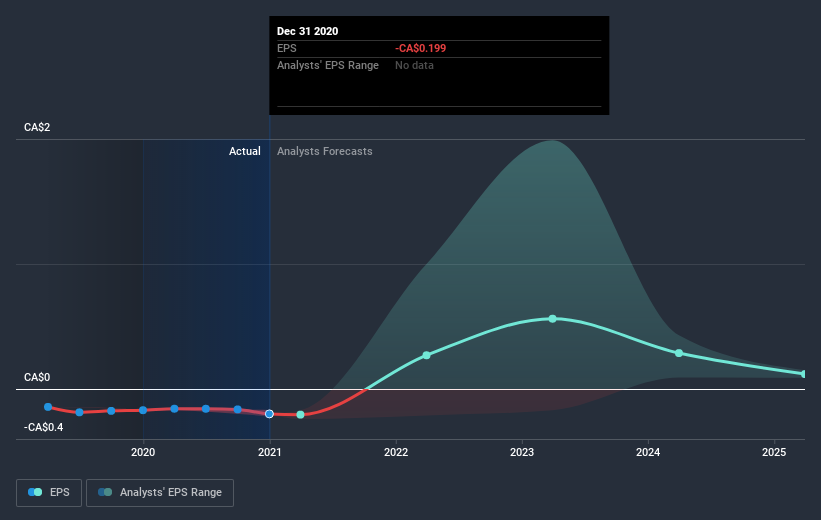

We feel now is a pretty good time to analyse Appili Therapeutics Inc.’s (TSE:APLI) business as it appears the company may be on the cusp of a considerable accomplishment. Appili Therapeutics Inc., a biopharmaceutical company, acquires, develops, and commercializes novel medicines for unmet needs in the infectious disease in Canada. With the latest financial year loss of CA$5.4m and a trailing-twelve-month loss of CA$11m, the CA$64m market-cap company amplified its loss by moving further away from its breakeven target. Many investors are wondering about the rate at which Appili Therapeutics will turn a profit, with the big question being “when will the company breakeven?” We’ve put together a brief outline of industry analyst expectations for the company, its year of breakeven and its implied growth rate.

Appili Therapeutics is bordering on breakeven, according to the 5 Canadian Pharmaceuticals analysts. They anticipate the company to incur a final loss in 2021, before generating positive profits of CA$19m in 2022. Therefore, the company is expected to breakeven just over a year from now. How fast will the company have to grow each year in order to reach the breakeven point by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 41% year-on-year, on average, which is rather optimistic! Should the business grow at a slower rate, it will become profitable at a later date than expected.

Underlying developments driving Appili Therapeutics’ growth isn’t the focus of this broad overview, though, bear in mind that by and large a pharma company has lumpy cash flows which are contingent on the drug and stage of product development the business is in. So, a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one aspect worth mentioning. The company has managed its capital judiciously, with debt making up 6.0% of equity. This means that it has predominantly funded its operations from equity capital, and its low debt obligation reduces the risk around investing in the loss-making company.