David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Magnite, Inc. (NASDAQ:MGNI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Magnite’s Debt?

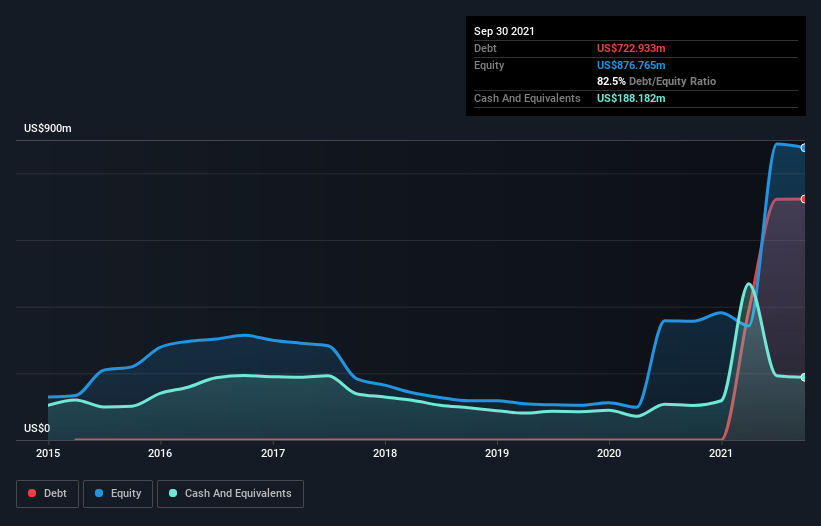

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Magnite had US$722.9m of debt, an increase on none, over one year. On the flip side, it has US$188.2m in cash leading to net debt of about US$534.8m.

How Strong Is Magnite’s Balance Sheet?

The latest balance sheet data shows that Magnite had liabilities of US$858.9m due within a year, and liabilities of US$797.4m falling due after that. Offsetting these obligations, it had cash of US$188.2m as well as receivables valued at US$765.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$703.1m.

Magnite has a market capitalization of US$2.23b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Magnite can strengthen its balance sheet over time.

Over 12 months, Magnite reported revenue of US$389m, which is a gain of 107%, although it did not report any earnings before interest and tax. So there’s no doubt that shareholders are cheering for growth

Caveat Emptor

Even though Magnite managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. To be specific the EBIT loss came in at US$38m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. On the bright side, we note that trailing twelve month EBIT is worse than the free cash flow of US$37m and the profit of US$5.5m. So one might argue that there’s still a chance it can get things on the right track.