The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Lantronix, Inc. (NASDAQ:LTRX) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Lantronix Carry?

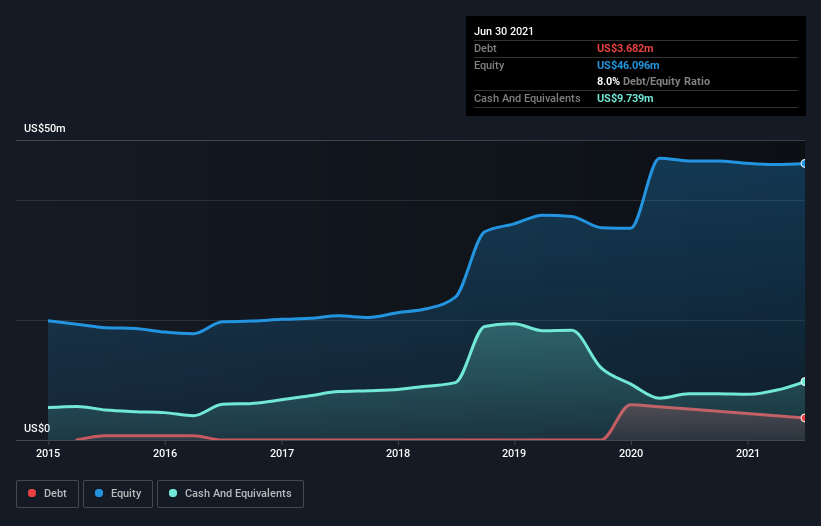

The image below, which you can click on for greater detail, shows that Lantronix had debt of US$3.68m at the end of June 2021, a reduction from US$5.15m over a year. However, its balance sheet shows it holds US$9.74m in cash, so it actually has US$6.06m net cash.

A Look At Lantronix’s Liabilities

The latest balance sheet data shows that Lantronix had liabilities of US$22.9m due within a year, and liabilities of US$3.61m falling due after that. On the other hand, it had cash of US$9.74m and US$15.5m worth of receivables due within a year. So its liabilities total US$1.26m more than the combination of its cash and short-term receivables.

Having regard to Lantronix’s size, it seems that its liquid assets are well balanced with its total liabilities. So it’s very unlikely that the US$179.3m company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Lantronix also has more cash than debt, so we’re pretty confident it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Lantronix can strengthen its balance sheet over time.

In the last year Lantronix wasn’t profitable at an EBIT level, but managed to grow its revenue by 19%, to US$71m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Lantronix?

Although Lantronix had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$3.5m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. With revenue growth uninspiring, we’d really need to see some positive EBIT before mustering much enthusiasm for this business. T