Summary

- Kuaishou Technology’s share price is at its lowest since the company’s IPO, and this is due to both the valuation de-rating of technology stocks and news of its competitor’s IPO.

- Kuaishou Technology’s FY 2020 revenue growth was in line with market expectations, and its online marketing services and other services (e-commerce) business lines grew rapidly last year.

- Kuaishou Technology is valued by the market at consensus forward FY 2021 and FY 2022 Enterprise Value-to-Revenue multiples of 11.4 times and 7.9 times, respectively.

Elevator Pitch

I have a Neutral rating for Kuaishou Technology (OTCPK:KUASF) [1024:HK].

On one hand, Kuaishou Technology’s current share price is at its lowest since the company’s IPO in early-February 2021. This is largely due to both the valuation de-rating of technology stocks and news of its larger competitor’s potential IPO. These two factors could still be a drag on Kuaishou Technology’s stock price in the near term. Notably, Kuaishou Technology is valued by the market at a premium to the majority of its listed peers at consensus forward FY 2021 and FY 2022 Enterprise Value-to-Revenue multiples of 11.4 times and 7.9 times, respectively.

On the other hand, Kuaishou Technology’s FY 2020 revenue growth was in line with market expectations, and its online marketing services and other services (e-commerce) business lines grew rapidly last year. This will help to partially alleviate the market’s concerns about the company’s reliance on revenue derived from its core livestreaming (i.e. virtual gifts) business line, which is exposed to regulatory headwinds.

I think that a Neutral rating is fair for Kuaishou Technology, considering the various factors highlighted above.

Kuaishou Technology’s shares are listed on both the OTC market and the Hong Kong Stock Exchange. But Kuaishou Technology’s OTC shares with the KUASF ticker have limited trading liquidity, as the average daily trading value of the OTC shares since its IPO is below $10,000. In contrast, the average daily trading value for Kuaishou Technology’s Hong Kong-listed shares with the 1024:HK ticker since the company’s listing was more than $200 million. Investors can deal in Hong Kong-listed shares with US stockbrokers providing access to Asian markets such as Interactive Brokers.

Company Description

Kuaishou Technology calls itself “the largest live streaming platform” and “the second largest short video” & “live streaming e-commerce platform” in the world in the company’s IPO prospectus published in January 2021. The company was started in 2011 in China, and listed on the Hong Kong Stock Exchange on February 5, 2021. Chinese internet company Tencent Holdings Limited (OTCPK:TCEHY) (OTCPK:TCTZF) [700:HK] is Kuaishou Technology’s largest shareholder with a 21% equity interest based on S&P Capital IQ data.

The company derived 57% and 37% of its FY 2020 revenue from its live streaming and online marketing services business lines, respectively. Other services, mainly e-commerce, contributed the remaining 6% of Kuaishou Technology’s top line in the most recent fiscal year.

Stock Drops To New Share Price Low Since IPO

Kuaishou Technology’s share price closed at HK$240 as of April 15, 2021, which is the lowest the company’s stock price has been since its IPO on February 5, 2021. The company’s IPO offering price was $115, and the stock’s closing price was $300.00 on the first day of trading. Kuaishou Technology subsequently traded as high as $415 on February 17, 2021, prior to declining -42% from its peak in the next two months.

It is no surprise that Kuaishou Technology’s share price has corrected significantly in the past two months, as Chinese technology stocks in general have suffered from a valuation de-rating during the same period. Notably, the Hang Seng Tech Index, which comprises of the largest technology names listed in Hong Kong, also fell by -26% between February 17, 2021 and April 15, 2021.

However, it is noteworthy that Kuaishou Technology’s stock price dropped by -8% from HK$260.20 as of April 14, 2021 to HK$240.00 as of April 15, 2021. On the same day, the Hang Seng Tech Index only declined marginally by -1%. Kuaishou Technology’s poor share price performance on April 15, 2021 is likely attributable to news of its competitor’s plans to list on the Hong Kong Stock Exchange.

Chinese media Caixin Global reported on April 14, 2021 that “ByteDance Ltd. has chosen instead to IPO on the Hong Kong Stock Exchange (rather than list in the US) and will file its prospectus in the second quarter” of 2021.

The potential IPO of ByteDance in Hong Kong is negative for Kuaishou Technology, as investors could potentially sell Kuaishou Technology’s shares and buy ByteDance’s shares in the future assuming ByteDance lists successfully on the Hong Kong Stock Exchange.

There are two key reasons why investors could possibly prefer ByteDance over Kuaishou Technology.

Firstly, ByteDance is the larger of the two companies in terms of both user base and valuation.

ByteDance’s Douyin (which is referred to TikTok outside of China) is the largest short video platform in China and globally in terms of daily active users. Kuaishou Technology’s current market capitalization is approximately $128 billion, while ByteDance’s private market valuation is speculated to be above $250 billion. For investors seeking a listed proxy for the growing short video market, they could opt for the market leader, ByteDance, which could result in further selling pressure for Kuaishou Technology’s shares in time to come.

Secondly, ByteDance might also prove to a better company than Kuaishou Technology on other metrics apart from size, which could lead to investors favoring the former. As ByteDance is currently a private company, there are insufficient public disclosures to compare the two companies on financial ratios and user engagement statistics, but that will no longer be the case once ByteDance is listed.

For example, ByteDance has gained more traction in overseas markets. A January 28, 2021 Nikkei Asia news article highlighted that Kuaishou Technology has “been less successful” than ByteDance in the “international market.” Kuaishou Technology also acknowledged at the company’s FY 2020 earnings call on March 23, 2021 that “it is still in a very early stage” of overseas expansion”, and noted that “there is still not much commercialization and there isn’t really revenue contribution” from overseas markets.

In a nutshell, Kuaishou Technology’s share price could continue to be under pressure in the near term, with the continued valuation de-rating of technology & growth stocks in general, and the potential IPO of its closest rival, ByteDance.

Spotlight On Change In Revenue Mix

It is not all doom and gloom for Kuaishou Technology. The company announced its FY 2020 financial results on March 23, 2021, and its revenue growth last year was in line with market expectations.

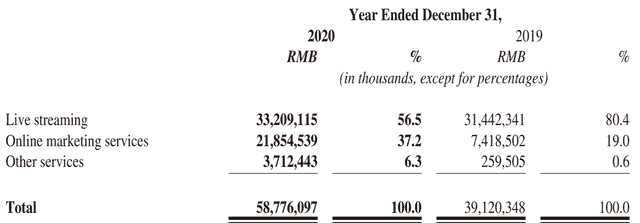

Kuaishou Technology’s top line jumped by +50% YoY from RMB39,120 million in FY 2019 to RMB58,776 million in FY 2020. This was slightly better than the sell-side analysts’ consensus full-year 2020 revenue forecast of approximately RMB58.6 billion.

More importantly, there was a significant change in Kuaishou Technology’s revenue mix in FY 2020 as compared to FY 2019, as per the table below. The company is no longer as reliant as on live streaming as it was in the past, and its revenue from online marketing services and other services (e-commerce) are growing rapidly.

Kuaishou Technology’s Revenue Mix For FY 2020 And FY 2019

Nikkei Asia noted in a January 2021 commentary that “virtual gifting (from livestreaming) is declining as a share of overall revenue” for Kuaishou Technology with Chinese regulatory authorities “ordered that hosts and gift givers on live-streaming platforms register their real names and banned teenagers from gifting” in late-2020. This makes it even more important for Kuaishou Technology to diversify its revenue streams beyond its core live streaming business line.

As a result, it is encouraging that Kuaishou Technology’s revenue from online marketing services almost tripled YoY to RMB21.9 billion in FY 2020, while its sales from other services (e-commerce) surged from RMB260 million in FY 2019 to RMB3,712 million in the most recent fiscal year.

Looking ahead, Kuaishou Technology has guided that the proportion of revenue contribution from its online marketing services business line should continue to increase going forward, and it also expects the future revenue growth for the online marketing services business line to be much faster than the industry’s average growth rate. The company cited key growth initiatives for this business line such as having “more interactive elements (incorporated) into the content and format of advertising”, improving its “brand marketing capabilities”, and increasing the size of its “sales team” at its recent FY 2020 results briefing in late-March 2021.

Kuaishou Technology’s e-commerce GMV (Gross Merchandise Value) also expanded significantly from RMB60 billion in FY 2019 to RMB381 billion in FY 2020, which was the key driver of the 13-fold increase in revenue for the company’s other services business line last year. With other services only representing 6% of the company’s FY 2020 revenue, there is significant room for growth with respect to Kuaishou Technology’s e-commerce business. At its recent earnings call last month, Kuaishou Technology stressed that its e-commerce business “is still in a very early stage of development”, with future growth driven by an increase in the number of product categories and merchants.

The future growth prospects for Kuaishou Technology are decent, with market consensus seeing the company delivering YoY revenue growth rates of +50% and +45% for FY 2021 and FY 2022, respectively. Apart from strong growth momentum for its online marketing services and other services (e-commerce) as highlighted above, it is also positive that Kuaishou Technology is witnessing increased user engagement with the average time spent by its active users every day growing by +17% to 87.3 minutes last year. Sell-side analysts also forecast that Kuaishou Technology will be profitably by FY 2022.

Valuation And Risk Factors

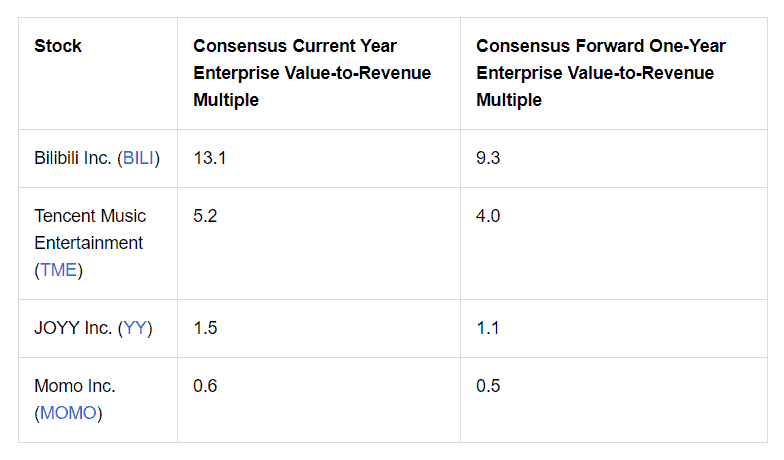

Kuaishou Technology trades at consensus forward FY 2021 and FY 2022 Enterprise Value-to-Revenue multiples of 11.4 times and 7.9 times, respectively based on its share price of HK$240 as of April 15, 2021. This seems rather expensive on an absolute basis.

The market values Kuaishou Technology at a premium to most of its peers, but the companies listed in the table are not perfect peer comparables as they either operate in other business lines or have a different revenue mix. ByteDance is still the most appropriate peer comparable for Kuaishou Technology, so it will be worthy to track ByteDance’s IPO progress and see how the two companies stack up in terms of valuation.

Peer Valuation Comparison For Kuaishou Technology

I have sourced the forward-looking sell-side revenue estimates used in this article from S&P Capital IQ.

The key risk factors for Kuaishou Technology are slower-than-expected growth for its online marketing services and other services (e-commerce) business lines going forward, a deterioration in user engagement metrics in the future, a longer-than-expected time taken for the company to turn profitable, and new regulations & policies which have a negative impact on the company’s various business lines.

Asia Value & Moat Stocks is a research service for value investors seeking value stocks with a huge gap between price and intrinsic value, leaning towards deep value balance sheet bargains (i.e. buying assets at a discount e.g. net cash stocks, net-nets, low P/B stocks, sum-of-the-parts discounts) and wide moat stocks (i.e. buying earnings power at a discount in great companies like “Magic Formula” stocks, high-quality businesses, hidden champions and wide moat compounders). Sign up here to get started today!