Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Korn Ferry (NYSE:KFY) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Korn Ferry Carry?

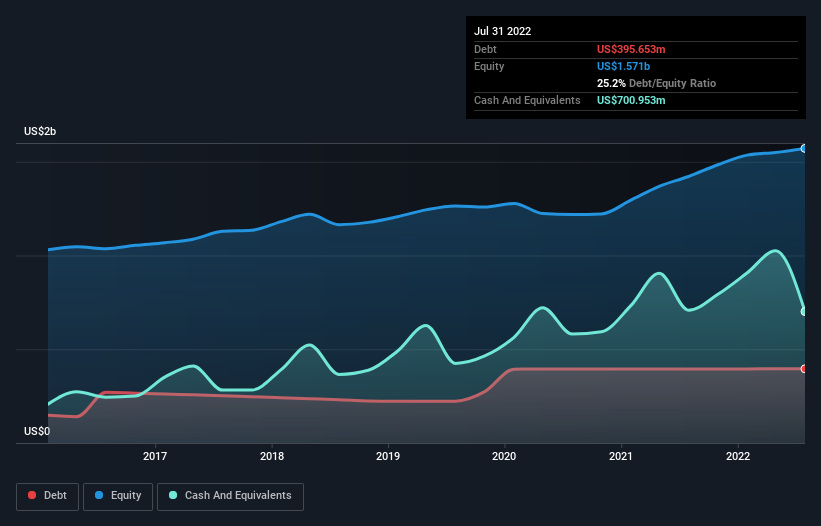

As you can see below, Korn Ferry had US$395.7m of debt, at July 2022, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$701.0m in cash, so it actually has US$305.3m net cash.

How Healthy Is Korn Ferry’s Balance Sheet?

We can see from the most recent balance sheet that Korn Ferry had liabilities of US$686.1m falling due within a year, and liabilities of US$946.8m due beyond that. Offsetting these obligations, it had cash of US$701.0m as well as receivables valued at US$672.2m due within 12 months. So its liabilities total US$259.6m more than the combination of its cash and short-term receivables.

Given Korn Ferry has a market capitalization of US$2.94b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Korn Ferry also has more cash than debt, so we’re pretty confident it can manage its debt safely.

In addition to that, we’re happy to report that Korn Ferry has boosted its EBIT by 65%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Korn Ferry’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Korn Ferry may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Korn Ferry generated free cash flow amounting to a very robust 84% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Summing Up

We could understand if investors are concerned about Korn Ferry’s liabilities, but we can be reassured by the fact it has has net cash of US$305.3m. And it impressed us with free cash flow of US$373m, being 84% of its EBIT. So we don’t think Korn Ferry’s use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start.