David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that World Fuel Services Corporation (NYSE:INT) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does World Fuel Services Carry?

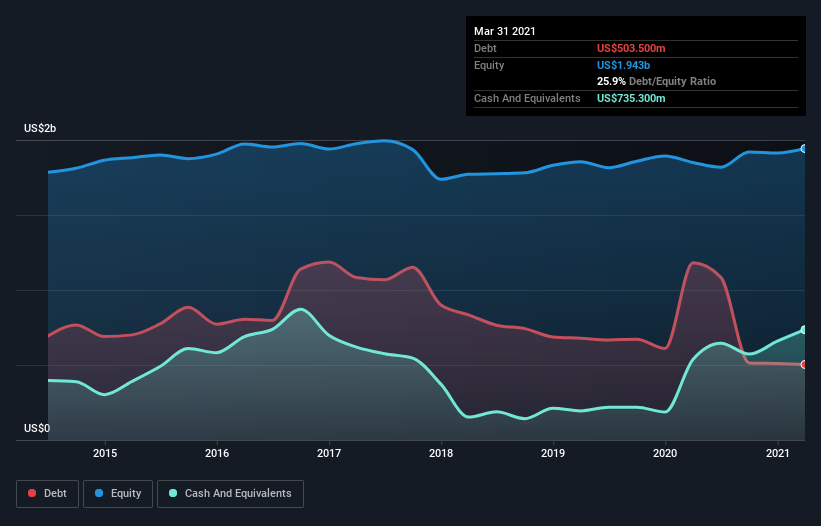

You can click the graphic below for the historical numbers, but it shows that World Fuel Services had US$466.5m of debt in March 2021, down from US$1.18b, one year before. However, its balance sheet shows it holds US$735.3m in cash, so it actually has US$268.8m net cash.

A Look At World Fuel Services’ Liabilities

Zooming in on the latest balance sheet data, we can see that World Fuel Services had liabilities of US$2.09b due within 12 months and liabilities of US$890.2m due beyond that. Offsetting these obligations, it had cash of US$735.3m as well as receivables valued at US$1.67b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$577.9m.

While this might seem like a lot, it is not so bad since World Fuel Services has a market capitalization of US$2.01b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, World Fuel Services also has more cash than debt, so we’re pretty confident it can manage its debt safely.

Shareholders should be aware that World Fuel Services’s EBIT was down 56% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if World Fuel Services can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. World Fuel Services may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, World Fuel Services actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

Although World Fuel Services’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$268.8m. And it impressed us with free cash flow of US$662m, being 105% of its EBIT. So we are not troubled with World Fuel Services’s debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.