The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Werner Enterprises, Inc. (NASDAQ:WERN) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Werner Enterprises Carry?

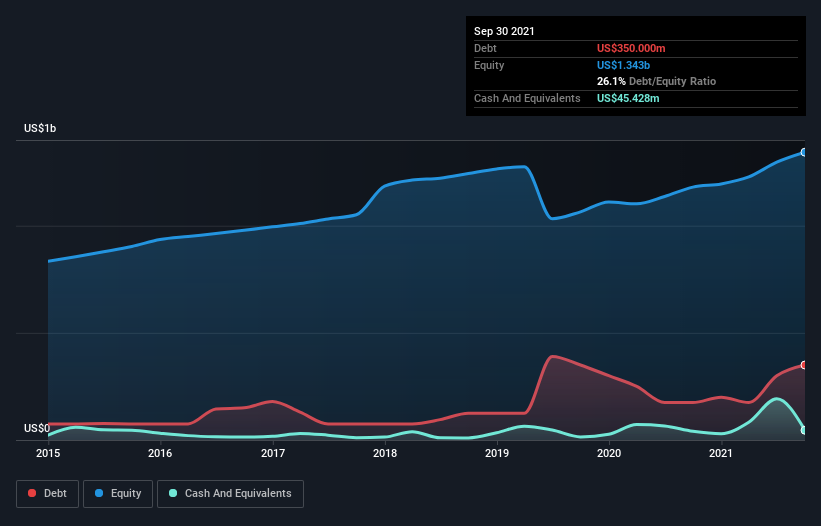

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Werner Enterprises had US$350.0m of debt, an increase on US$175.0m, over one year. However, because it has a cash reserve of US$45.4m, its net debt is less, at about US$304.6m.

A Look At Werner Enterprises’ Liabilities

We can see from the most recent balance sheet that Werner Enterprises had liabilities of US$261.2m falling due within a year, and liabilities of US$874.7m due beyond that. Offsetting these obligations, it had cash of US$45.4m as well as receivables valued at US$462.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$628.5m.https://d488687ff2062e747d93be580360dcf2.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

This deficit isn’t so bad because Werner Enterprises is worth US$3.12b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Werner Enterprises’s net debt is only 0.59 times its EBITDA. And its EBIT easily covers its interest expense, being 121 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, Werner Enterprises grew its EBIT by 31% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Werner Enterprises can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Werner Enterprises barely recorded positive free cash flow, in total. While many companies do operate at break-even, we prefer see substantial free cash flow, especially if a it already has dead.

Our View

Happily, Werner Enterprises’s impressive interest cover implies it has the upper hand on its debt. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that Werner Enterprises can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet.