Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Under Armour, Inc. (NYSE:UAA) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Under Armour’s Net Debt?

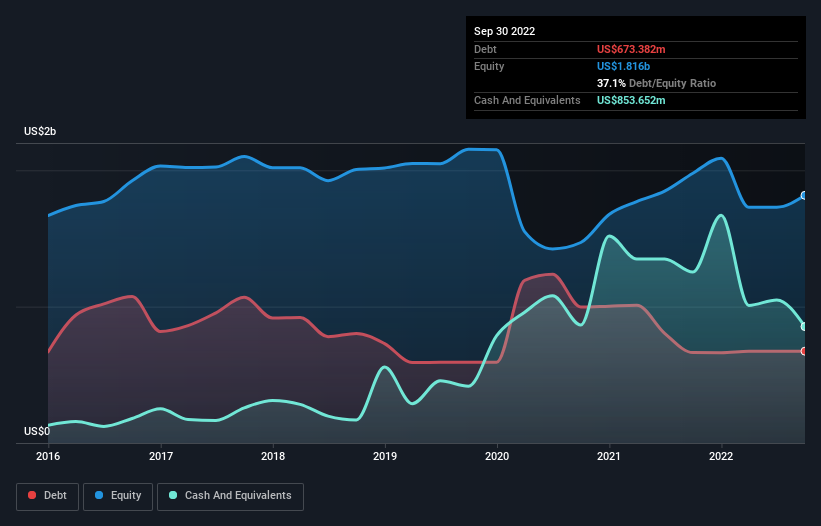

The chart below, which you can click on for greater detail, shows that Under Armour had US$673.4m in debt in September 2022; about the same as the year before. But it also has US$853.7m in cash to offset that, meaning it has US$180.3m net cash.

A Look At Under Armour’s Liabilities

We can see from the most recent balance sheet that Under Armour had liabilities of US$1.47b falling due within a year, and liabilities of US$1.48b due beyond that. Offsetting these obligations, it had cash of US$853.7m as well as receivables valued at US$782.1m due within 12 months. So it has liabilities totalling US$1.32b more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Under Armour is worth US$4.04b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, Under Armour also has more cash than debt, so we’re pretty confident it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Under Armour can strengthen its balance sheet over time.

Over 12 months, Under Armour made a loss at the EBIT level, and saw its revenue drop to US$5.2b, which is a fall of 5.9%. We would much prefer see growth.

So How Risky Is Under Armour?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Under Armour had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$1.9b of cash and made a loss of US$316m. With only US$180.3m on the balance sheet, it would appear that its going to need to raise capital again soon. Summing up, we’re a little skeptical of this one, as it seems fairly risky in the absence of free cashflow.