David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Travelzoo (NASDAQ:TZOO) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Travelzoo’s Debt?

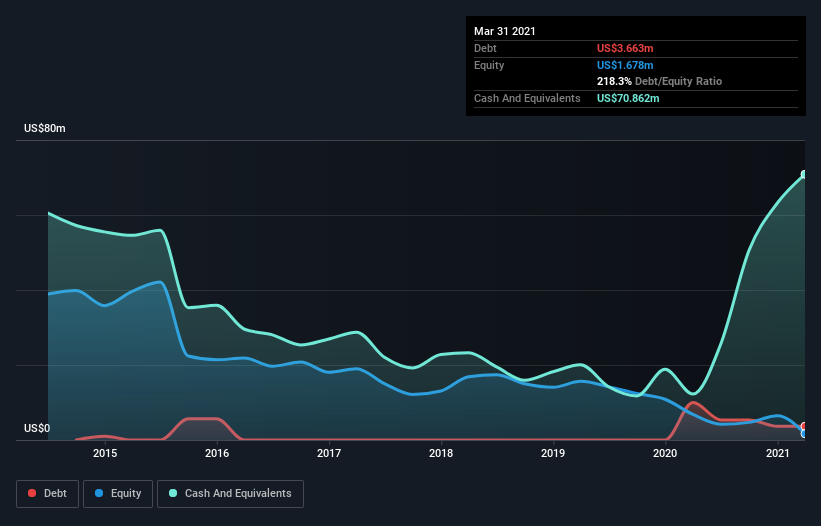

As you can see below, Travelzoo had US$3.66m of debt at March 2021, down from US$9.97m a year prior. But it also has US$70.9m in cash to offset that, meaning it has US$67.2m net cash.

How Healthy Is Travelzoo’s Balance Sheet?

The latest balance sheet data shows that Travelzoo had liabilities of US$100.1m due within a year, and liabilities of US$13.0m falling due after that. On the other hand, it had cash of US$70.9m and US$7.29m worth of receivables due within a year. So it has liabilities totalling US$35.0m more than its cash and near-term receivables, combined.

Of course, Travelzoo has a market capitalization of US$191.3m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Travelzoo boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Travelzoo can strengthen its balance sheet over time.

In the last year Travelzoo had a loss before interest and tax, and actually shrunk its revenue by 51%, to US$48m. That makes us nervous, to say the least.

So How Risky Is Travelzoo?

While Travelzoo lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$59m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. Until we see some positive EBIT, we’re a bit cautious of the stock, not least because of the rather modest revenue growth. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.