The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, The Southern Company (NYSE:SO) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

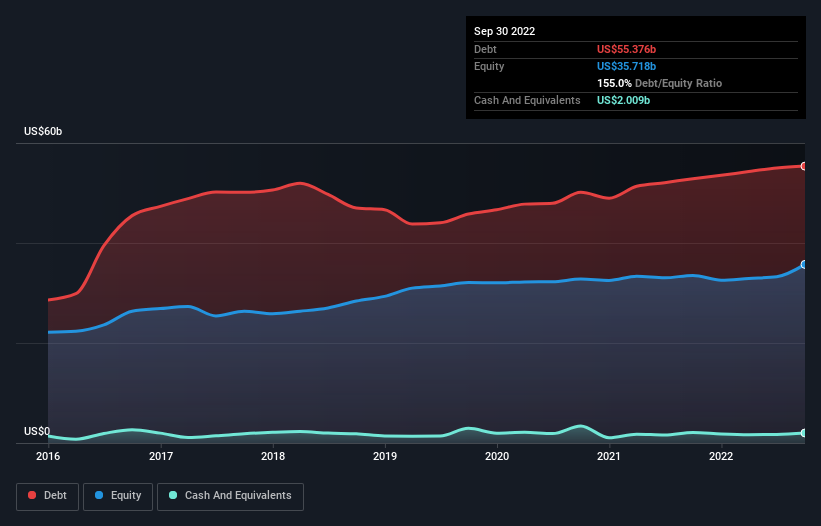

What Is Southern’s Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2022 Southern had US$55.4b of debt, an increase on US$52.9b, over one year. However, it does have US$2.01b in cash offsetting this, leading to net debt of about US$53.4b.

How Strong Is Southern’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Southern had liabilities of US$12.8b due within 12 months and liabilities of US$85.5b due beyond that. Offsetting this, it had US$2.01b in cash and US$3.27b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$93.0b.

When you consider that this deficiency exceeds the company’s huge US$72.8b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Southern has a rather high debt to EBITDA ratio of 5.6 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 2.8 times, suggesting it can responsibly service its obligations. The good news is that Southern improved its EBIT by 7.7% over the last twelve months, thus gradually reducing its debt levels relative to its earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Southern can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Southern saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Southern’s net debt to EBITDA left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But at least it’s pretty decent at growing its EBIT; that’s encouraging. It’s also worth noting that Southern is in the Electric Utilities industry, which is often considered to be quite defensive. Overall, it seems to us that Southern’s balance sheet is really quite a risk to the business. For this reason we’re pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start.