Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies SM Energy Company (NYSE:SM) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

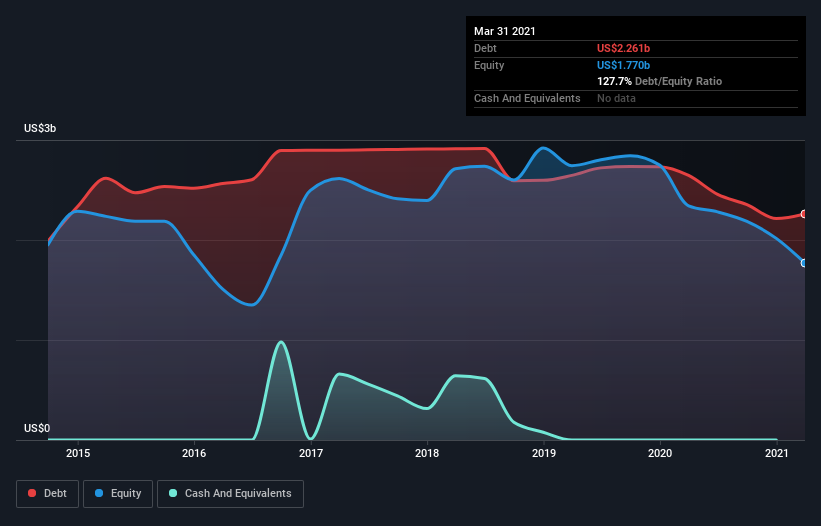

What Is SM Energy’s Net Debt?

You can click the graphic below for the historical numbers, but it shows that SM Energy had US$2.25b of debt in March 2021, down from US$2.65b, one year before. And it doesn’t have much cash, so its net debt is about the same.

A Look At SM Energy’s Liabilities

The latest balance sheet data shows that SM Energy had liabilities of US$776.6m due within a year, and liabilities of US$2.47b falling due after that. On the other hand, it had cash of US$10.0k and US$199.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.05b.

When you consider that this deficiency exceeds the company’s US$2.33b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if SM Energy can strengthen its balance sheet over time.

In the last year SM Energy had a loss before interest and tax, and actually shrunk its revenue by 24%, to US$1.2b. To be frank that doesn’t bode well.

Caveat Emptor

While SM Energy’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping US$799m. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. For example, we would not want to see a repeat of last year’s loss of US$604m. In the meantime, we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start.