Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, The Sherwin-Williams Company (NYSE:SHW) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Sherwin-Williams’s Debt?

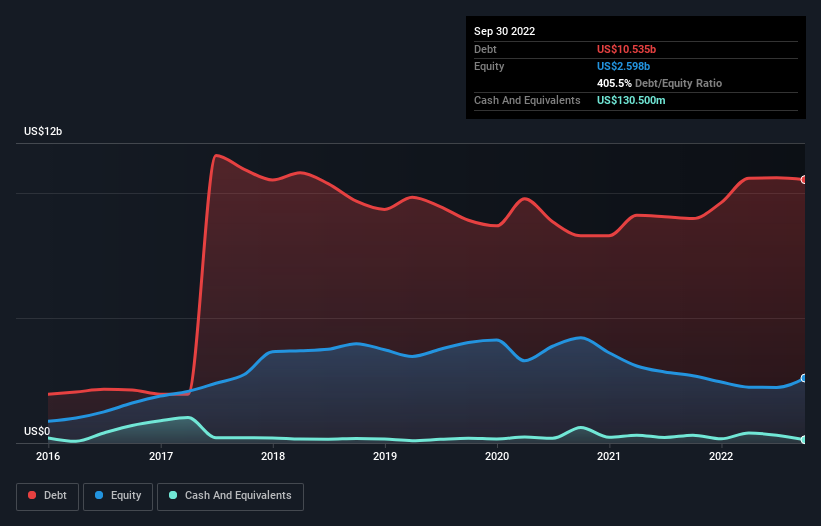

You can click the graphic below for the historical numbers, but it shows that as of September 2022 Sherwin-Williams had US$10.5b of debt, an increase on US$8.98b, over one year. And it doesn’t have much cash, so its net debt is about the same.

A Look At Sherwin-Williams’ Liabilities

Zooming in on the latest balance sheet data, we can see that Sherwin-Williams had liabilities of US$6.10b due within 12 months and liabilities of US$13.6b due beyond that. On the other hand, it had cash of US$130.5m and US$2.97b worth of receivables due within a year. So it has liabilities totalling US$16.5b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Sherwin-Williams has a huge market capitalization of US$64.0b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt to EBITDA of 3.1 Sherwin-Williams has a fairly noticeable amount of debt. On the plus side, its EBIT was 8.4 times its interest expense, and its net debt to EBITDA, was quite high, at 3.1. Sadly, Sherwin-Williams’s EBIT actually dropped 3.2% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Sherwin-Williams’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Sherwin-Williams recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

When it comes to the balance sheet, the standout positive for Sherwin-Williams was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren’t so heartening. For instance it seems like it has to struggle a bit handle its debt, based on its EBITDA,. When we consider all the elements mentioned above, it seems to us that Sherwin-Williams is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring.