Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Shenandoah Telecommunications Company (NASDAQ:SHEN) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Shenandoah Telecommunications’s Net Debt?

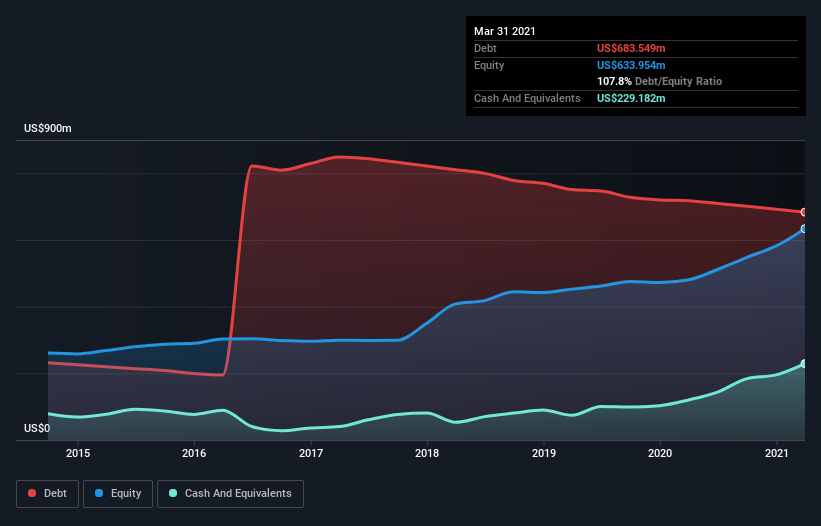

You can click the graphic below for the historical numbers, but it shows that Shenandoah Telecommunications had US$683.5m of debt in March 2021, down from US$717.7m, one year before. However, because it has a cash reserve of US$229.2m, its net debt is less, at about US$454.4m.

A Look At Shenandoah Telecommunications’ Liabilities

We can see from the most recent balance sheet that Shenandoah Telecommunications had liabilities of US$1.20b falling due within a year, and liabilities of US$246.0m due beyond that. Offsetting these obligations, it had cash of US$229.2m as well as receivables valued at US$66.6m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.15b.

This deficit isn’t so bad because Shenandoah Telecommunications is worth US$2.84b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

As it happens Shenandoah Telecommunications has a fairly concerning net debt to EBITDA ratio of 8.5 but very strong interest coverage of 1k. So either it has access to very cheap long term debt or that interest expense is going to grow! We also note that Shenandoah Telecommunications improved its EBIT from a last year’s loss to a positive US$3.2m. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Shenandoah Telecommunications’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Happily for any shareholders, Shenandoah Telecommunications actually produced more free cash flow than EBIT over the last year. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Shenandoah Telecommunications’s net debt to EBITDA was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its interest cover. When we consider all the elements mentioned above, it seems to us that Shenandoah Telecommunications is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.