David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Scorpio Tankers Inc. (NYSE:STNG) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Scorpio Tankers Carry?

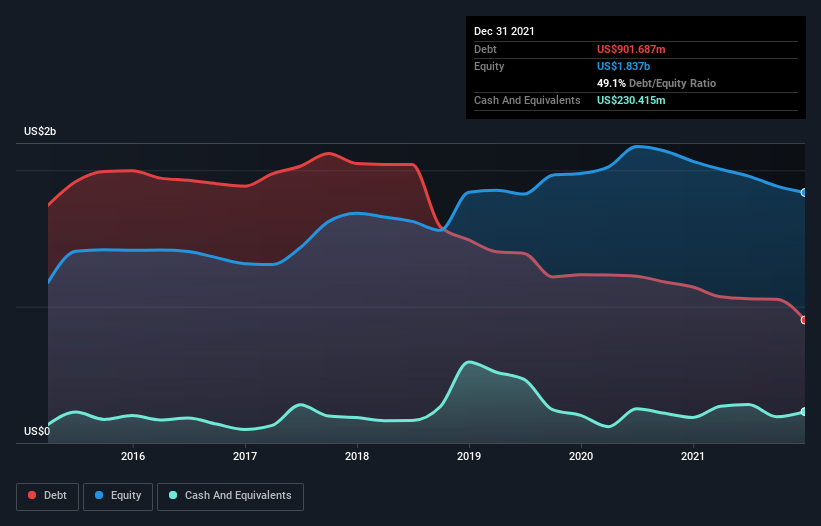

As you can see below, Scorpio Tankers had US$901.7m of debt at December 2021, down from US$1.14b a year prior. However, it also had US$230.4m in cash, and so its net debt is US$671.3m.

How Strong Is Scorpio Tankers’ Balance Sheet?

According to the last reported balance sheet, Scorpio Tankers had liabilities of US$527.8m due within 12 months, and liabilities of US$2.65b due beyond 12 months. Offsetting this, it had US$230.4m in cash and US$38.1m in receivables that were due within 12 months. So it has liabilities totalling US$2.91b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$1.18b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Scorpio Tankers would probably need a major re-capitalization if its creditors were to demand repayment. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Scorpio Tankers’s ability to maintain a healthy balance sheet going forward.

In the last year Scorpio Tankers had a loss before interest and tax, and actually shrunk its revenue by 41%, to US$541m. To be frank that doesn’t bode well.

Caveat Emptor

While Scorpio Tankers’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at US$91m. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. It’s fair to say the loss of US$234m didn’t encourage us either; we’d like to see a profit. In the meantime, we consider the stock to be risky.