The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that salesforce.com, inc. (NYSE:CRM) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is salesforce.com’s Debt?

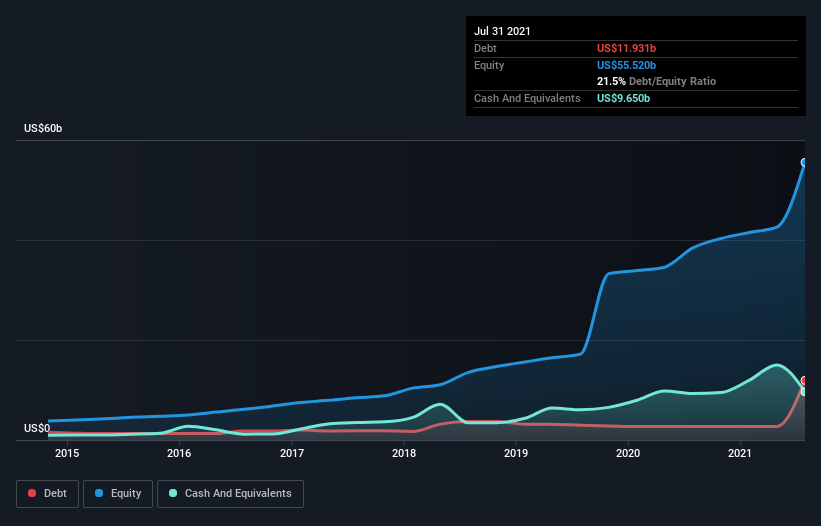

As you can see below, at the end of July 2021, salesforce.com had US$11.9b of debt, up from US$2.68b a year ago. Click the image for more detail. However, because it has a cash reserve of US$9.65b, its net debt is less, at about US$2.28b.

How Strong Is salesforce.com’s Balance Sheet?

The latest balance sheet data shows that salesforce.com had liabilities of US$17.4b due within a year, and liabilities of US$15.7b falling due after that. On the other hand, it had cash of US$9.65b and US$4.07b worth of receivables due within a year. So it has liabilities totalling US$19.4b more than its cash and near-term receivables, combined.

Of course, salesforce.com has a titanic market capitalization of US$269.5b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. But either way, salesforce.com has virtually no net debt, so it’s fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 0.64 times EBITDA, salesforce.com is arguably pretty conservatively geared. And it boasts interest cover of 8.1 times, which is more than adequate. Better yet, salesforce.com grew its EBIT by 981% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine salesforce.com’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, salesforce.com actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Happily, salesforce.com’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And the good news does not stop there, as its EBIT growth rate also supports that impression! Overall, we don’t think salesforce.com is taking any bad risks, as its debt load seems modest. So we’re not worried about the use of a little leverage on the balance sheet. There’s no doubt that we learn most about debt from the balance sheet.