Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Revance Therapeutics, Inc. (NASDAQ:RVNC) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Revance Therapeutics’s Debt?

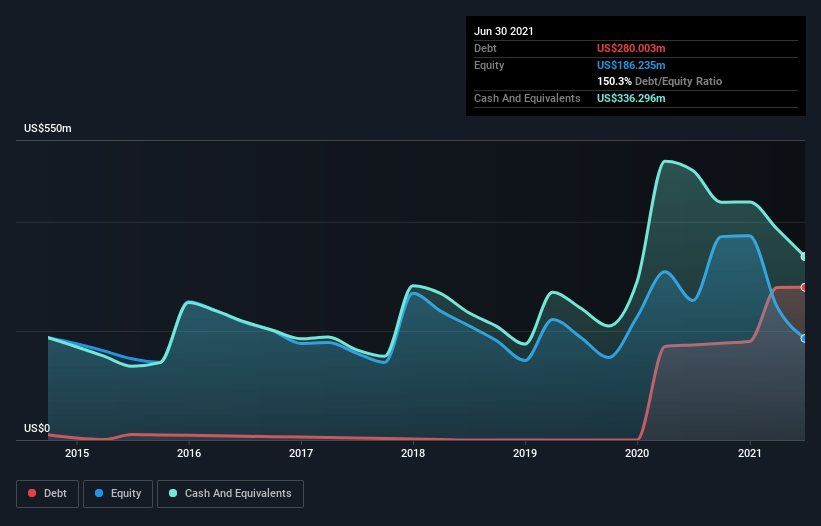

As you can see below, at the end of June 2021, Revance Therapeutics had US$280.0m of debt, up from US$174.3m a year ago. Click the image for more detail. However, it does have US$336.3m in cash offsetting this, leading to net cash of US$56.3m.

A Look At Revance Therapeutics’ Liabilities

We can see from the most recent balance sheet that Revance Therapeutics had liabilities of US$58.2m falling due within a year, and liabilities of US$396.4m due beyond that. Offsetting these obligations, it had cash of US$336.3m as well as receivables valued at US$641.0k due within 12 months. So its liabilities total US$117.7m more than the combination of its cash and short-term receivables.

Since publicly traded Revance Therapeutics shares are worth a total of US$1.86b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Revance Therapeutics also has more cash than debt, so we’re pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Revance Therapeutics’s ability to maintain a healthy balance sheet going forward.

In the last year Revance Therapeutics wasn’t profitable at an EBIT level, but managed to grow its revenue by 9,467%, to US$47m. When it comes to revenue growth, that’s like nailing the game winning 3-pointer!

So How Risky Is Revance Therapeutics?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Revance Therapeutics had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$250m and booked a US$303m accounting loss. But the saving grace is the US$56.3m on the balance sheet. That means it could keep spending at its current rate for more than two years. Importantly, Revance Therapeutics’s revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. The balance sheet is clearly the area to focus on when you are analysing debt.