Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Republic Services, Inc. (NYSE:RSG) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Republic Services Carry?

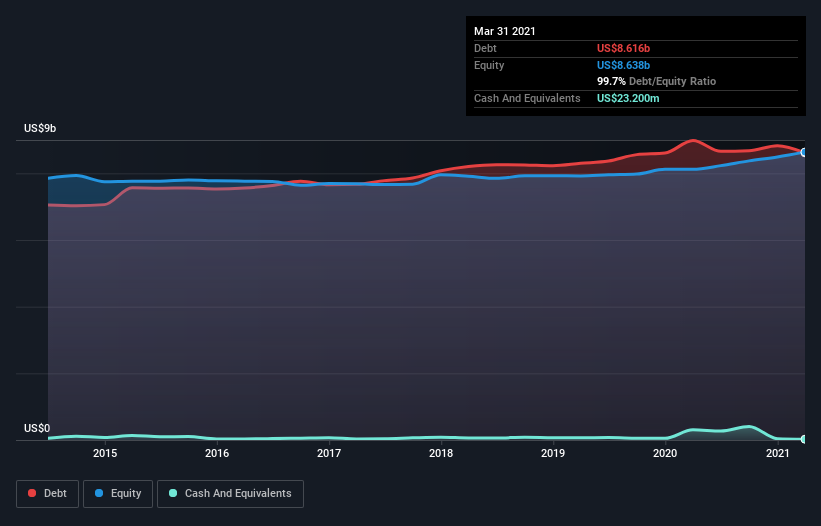

You can click the graphic below for the historical numbers, but it shows that Republic Services had US$8.62b of debt in March 2021, down from US$8.98b, one year before. Net debt is about the same, since the it doesn’t have much cash.

A Look At Republic Services’ Liabilities

The latest balance sheet data shows that Republic Services had liabilities of US$2.15b due within a year, and liabilities of US$12.5b falling due after that. On the other hand, it had cash of US$23.2m and US$1.26b worth of receivables due within a year. So its liabilities total US$13.3b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Republic Services has a huge market capitalization of US$35.0b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Republic Services’s debt is 2.8 times its EBITDA, and its EBIT cover its interest expense 5.9 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. We saw Republic Services grow its EBIT by 7.2% in the last twelve months. That’s far from incredible but it is a good thing, when it comes to paying off debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Republic Services’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Republic Services recorded free cash flow worth 67% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On our analysis Republic Services’s conversion of EBIT to free cash flow should signal that it won’t have too much trouble with its debt. But the other factors we noted above weren’t so encouraging. For example, its net debt to EBITDA makes us a little nervous about its debt. Considering this range of data points, we think Republic Services is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.