Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Reading International, Inc. (NASDAQ:RDI) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Reading International Carry?

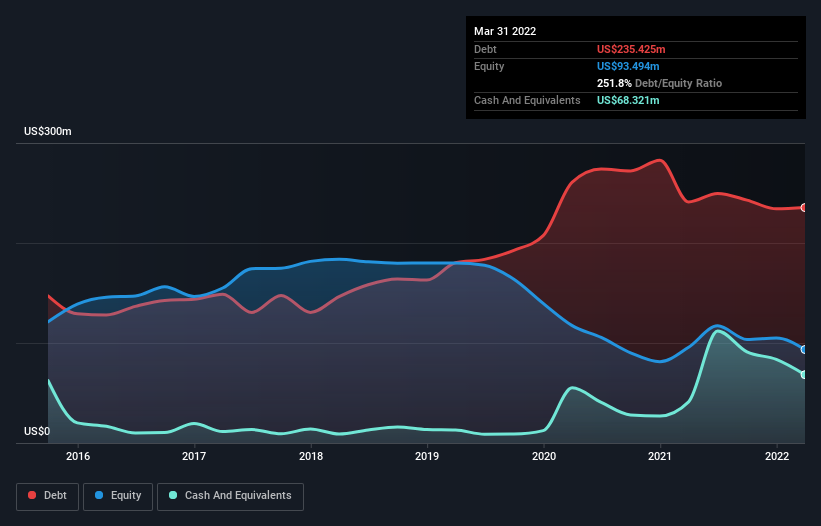

The chart below, which you can click on for greater detail, shows that Reading International had US$235.4m in debt in March 2022; about the same as the year before. However, it does have US$68.3m in cash offsetting this, leading to net debt of about US$167.1m.

How Healthy Is Reading International’s Balance Sheet?

The latest balance sheet data shows that Reading International had liabilities of US$139.1m due within a year, and liabilities of US$438.0m falling due after that. Offsetting these obligations, it had cash of US$68.3m as well as receivables valued at US$3.96m due within 12 months. So it has liabilities totalling US$504.8m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$127.6m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Reading International would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Reading International can strengthen its balance sheet over time.

Over 12 months, Reading International reported revenue of US$158m, which is a gain of 216%, although it did not report any earnings before interest and tax. That’s virtually the hole-in-one of revenue growth!

Caveat Emptor

Even though Reading International managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Indeed, it lost a very considerable US$36m at the EBIT level. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. Of course, it may be able to improve its situation with a bit of luck and good execution. Nevertheless, we would not bet on it given that it vaporized US$39m in cash over the last twelve months, and it doesn’t have much by way of liquid assets. So we think this stock is risky, like walking through a dirty dog park with a mask on. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.