Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, PPG Industries, Inc. (NYSE:PPG) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is PPG Industries’s Net Debt?

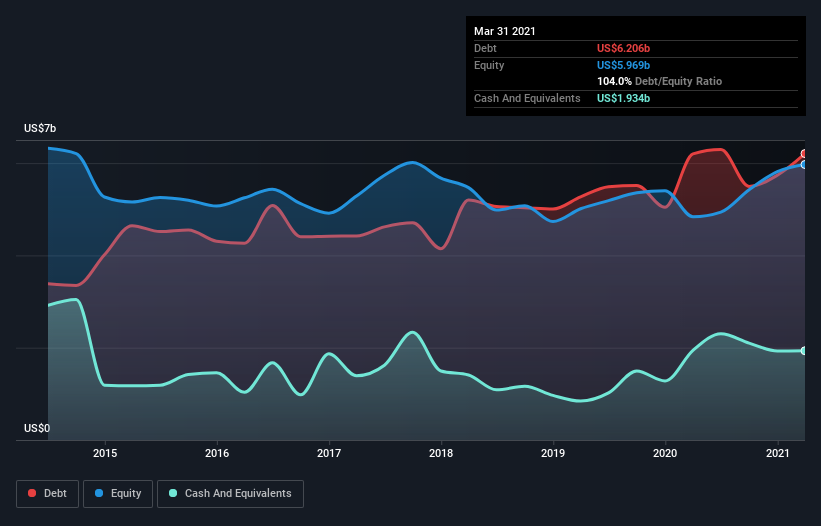

As you can see below, PPG Industries had US$6.21b of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$1.93b, its net debt is less, at about US$4.27b.

How Healthy Is PPG Industries’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that PPG Industries had liabilities of US$5.12b due within 12 months and liabilities of US$9.05b due beyond that. On the other hand, it had cash of US$1.93b and US$3.03b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$9.20b.

This deficit isn’t so bad because PPG Industries is worth a massive US$42.6b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

We’d say that PPG Industries’s moderate net debt to EBITDA ratio ( being 1.8), indicates prudence when it comes to debt. And its commanding EBIT of 16.3 times its interest expense, implies the debt load is as light as a peacock feather. We saw PPG Industries grow its EBIT by 8.5% in the last twelve months. That’s far from incredible but it is a good thing, when it comes to paying off debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if PPG Industries can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, PPG Industries generated free cash flow amounting to a very robust 88% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that PPG Industries’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Zooming out, PPG Industries seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.