Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Plexus Corp. (NASDAQ:PLXS) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Plexus Carry?

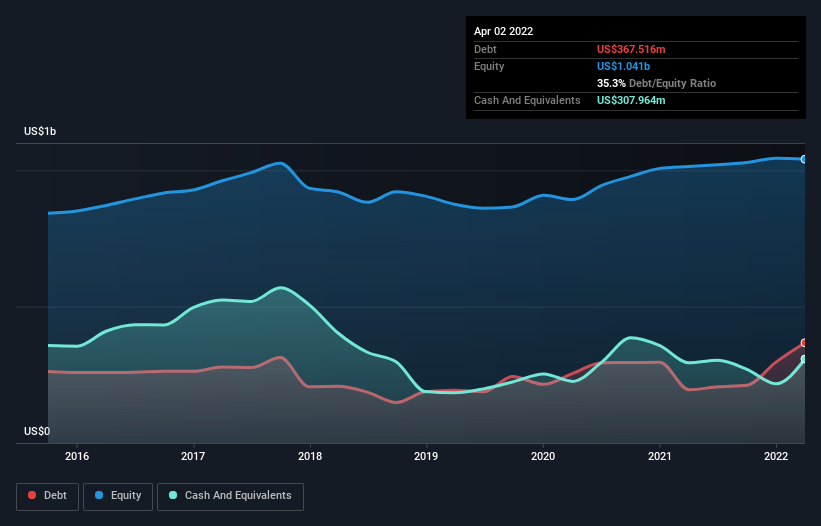

As you can see below, at the end of April 2022, Plexus had US$367.5m of debt, up from US$195.4m a year ago. Click the image for more detail. However, it also had US$308.0m in cash, and so its net debt is US$59.6m.

How Healthy Is Plexus’ Balance Sheet?

The latest balance sheet data shows that Plexus had liabilities of US$1.66b due within a year, and liabilities of US$290.3m falling due after that. Offsetting this, it had US$308.0m in cash and US$687.2m in receivables that were due within 12 months. So it has liabilities totalling US$954.3m more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Plexus is worth US$2.20b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Plexus has a low net debt to EBITDA ratio of only 0.28. And its EBIT easily covers its interest expense, being 12.8 times the size. So we’re pretty relaxed about its super-conservative use of debt. The modesty of its debt load may become crucial for Plexus if management cannot prevent a repeat of the 24% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Plexus’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Plexus recorded free cash flow worth 60% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Based on what we’ve seen Plexus is not finding it easy, given its EBIT growth rate, but the other factors we considered give us cause to be optimistic. There’s no doubt that its ability to to cover its interest expense with its EBIT is pretty flash. When we consider all the factors mentioned above, we do feel a bit cautious about Plexus’s use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt.