Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Plexus Corp. (NASDAQ:PLXS) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Plexus’s Debt?

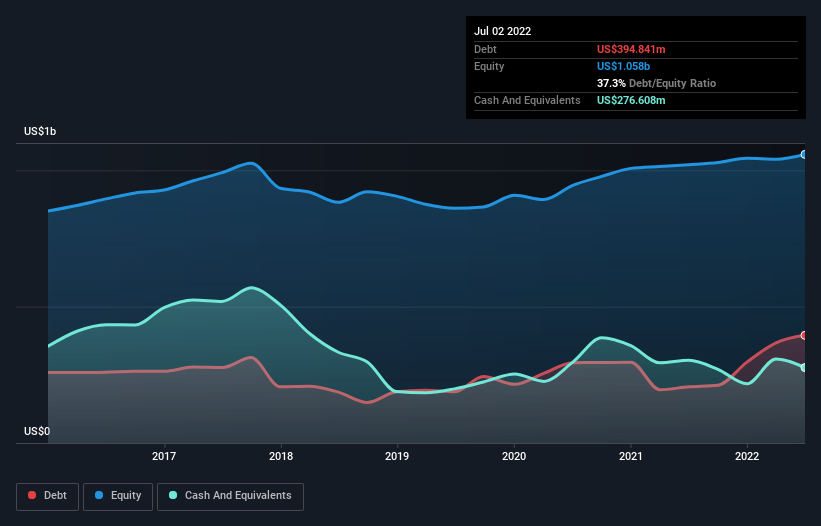

The image below, which you can click on for greater detail, shows that at July 2022 Plexus had debt of US$394.8m, up from US$206.1m in one year. However, it does have US$276.6m in cash offsetting this, leading to net debt of about US$118.2m.

How Healthy Is Plexus’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Plexus had liabilities of US$1.86b due within 12 months and liabilities of US$285.5m due beyond that. On the other hand, it had cash of US$276.6m and US$741.6m worth of receivables due within a year. So its liabilities total US$1.13b more than the combination of its cash and short-term receivables.

Plexus has a market capitalization of US$2.54b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Plexus has a low net debt to EBITDA ratio of only 0.53. And its EBIT easily covers its interest expense, being 13.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On the other hand, Plexus’s EBIT dived 14%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Plexus’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Plexus recorded free cash flow of 46% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Neither Plexus’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. Looking at all the angles mentioned above, it does seem to us that Plexus is a somewhat risky investment as a result of its debt. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of.