Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that The Pennant Group, Inc. (NASDAQ:PNTG) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Pennant Group’s Debt?

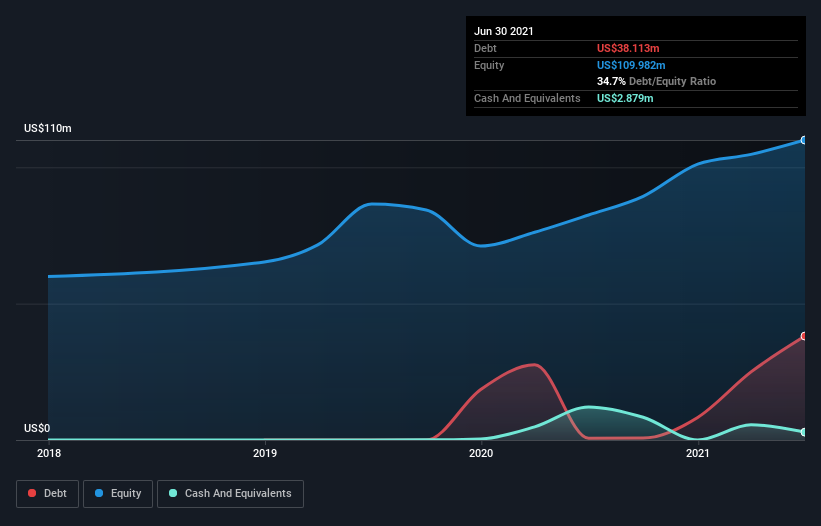

The image below, which you can click on for greater detail, shows that at June 2021 Pennant Group had debt of US$38.1m, up from US$642.0k in one year. However, it does have US$2.88m in cash offsetting this, leading to net debt of about US$35.2m.

How Strong Is Pennant Group’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Pennant Group had liabilities of US$82.8m due within 12 months and liabilities of US$337.0m due beyond that. Offsetting this, it had US$2.88m in cash and US$52.1m in receivables that were due within 12 months. So it has liabilities totalling US$364.8m more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Pennant Group is worth US$685.2m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

We’d say that Pennant Group’s moderate net debt to EBITDA ratio ( being 1.8), indicates prudence when it comes to debt. And its strong interest cover of 11.2 times, makes us even more comfortable. Importantly, Pennant Group’s EBIT fell a jaw-dropping 35% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Pennant Group’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Pennant Group recorded free cash flow worth 73% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Based on what we’ve seen Pennant Group is not finding it easy, given its EBIT growth rate, but the other factors we considered give us cause to be optimistic. There’s no doubt that its ability to to cover its interest expense with its EBIT is pretty flash. It’s also worth noting that Pennant Group is in the Healthcare industry, which is often considered to be quite defensive. When we consider all the factors mentioned above, we do feel a bit cautious about Pennant Group’s use of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase.