Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Paycom Software, Inc. (NYSE:PAYC) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Paycom Software’s Debt?

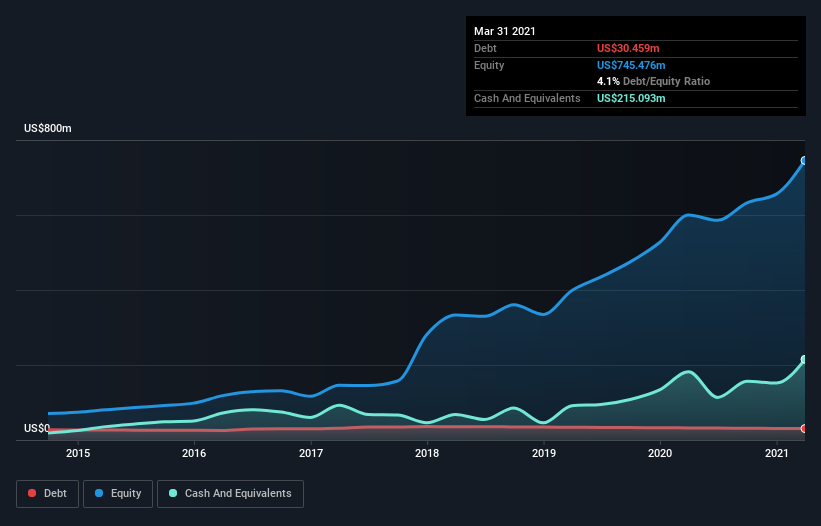

You can click the graphic below for the historical numbers, but it shows that Paycom Software had US$19.6m of debt in March 2021, down from US$32.2m, one year before. However, its balance sheet shows it holds US$215.1m in cash, so it actually has US$195.5m net cash.

How Strong Is Paycom Software’s Balance Sheet?

The latest balance sheet data shows that Paycom Software had liabilities of US$2.43b due within a year, and liabilities of US$235.7m falling due after that. Offsetting these obligations, it had cash of US$215.1m as well as receivables valued at US$19.8m due within 12 months. So its liabilities total US$2.43b more than the combination of its cash and short-term receivables.

Of course, Paycom Software has a titanic market capitalization of US$22.1b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Paycom Software also has more cash than debt, so we’re pretty confident it can manage its debt safely.

It is just as well that Paycom Software’s load is not too heavy, because its EBIT was down 24% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Paycom Software can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While Paycom Software has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Paycom Software recorded free cash flow worth 66% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While Paycom Software does have more liabilities than liquid assets, it also has net cash of US$195.5m. So we don’t have any problem with Paycom Software’s use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.