Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Oyster Point Pharma, Inc. (NASDAQ:OYST) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Oyster Point Pharma’s Net Debt?

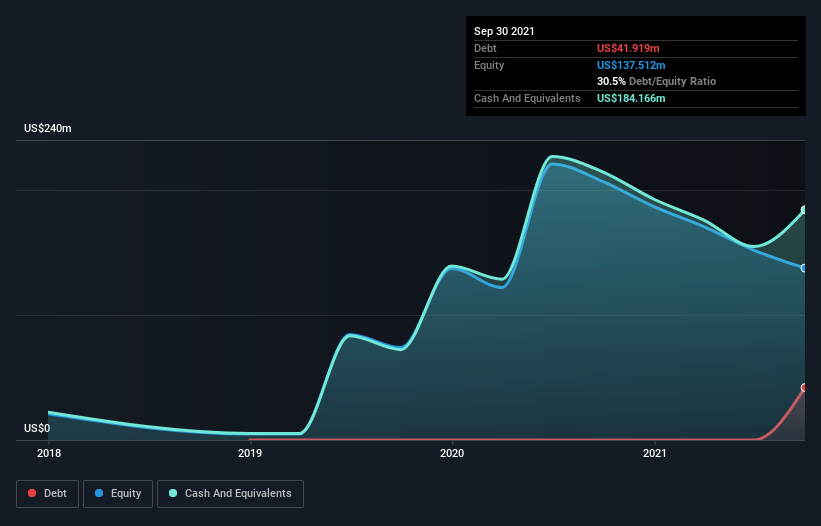

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Oyster Point Pharma had US$41.9m of debt, an increase on none, over one year. However, it does have US$184.2m in cash offsetting this, leading to net cash of US$142.2m.

A Look At Oyster Point Pharma’s Liabilities

The latest balance sheet data shows that Oyster Point Pharma had liabilities of US$15.2m due within a year, and liabilities of US$42.3m falling due after that. On the other hand, it had cash of US$184.2m and US$2.50m worth of receivables due within a year. So it actually has US$129.2m more liquid assets than total liabilities.

It’s good to see that Oyster Point Pharma has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Due to its strong net asset position, it is not likely to face issues with its lenders. Succinctly put, Oyster Point Pharma boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Oyster Point Pharma can strengthen its balance sheet over time.

In the last year Oyster Point Pharma managed to produce its first revenue as a listed company, but given the lack of profit, shareholders will no doubt be hoping to see some strong increases.

So How Risky Is Oyster Point Pharma?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Oyster Point Pharma had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$71m and booked a US$81m accounting loss. But the saving grace is the US$142.2m on the balance sheet. That means it could keep spending at its current rate for more than two years. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly. The balance sheet is clearly the area to focus on when you are analysing debt.