Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Occidental Petroleum Corporation (NYSE:OXY) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Occidental Petroleum’s Debt?

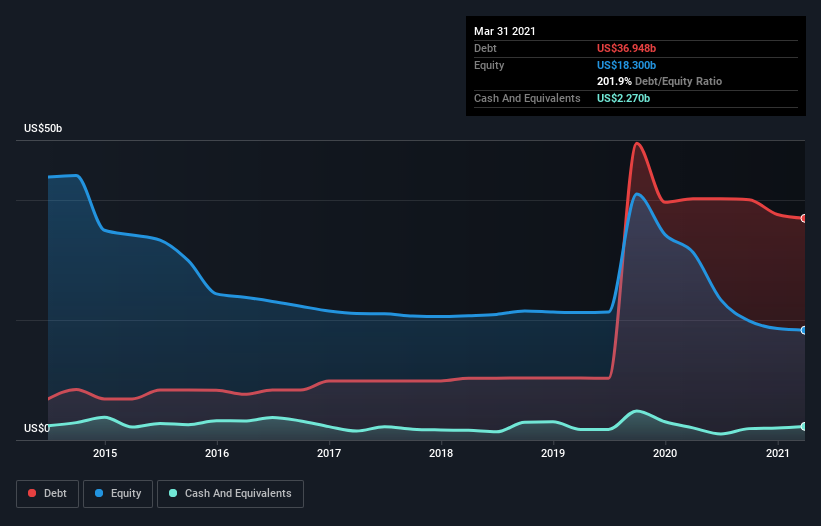

The image below, which you can click on for greater detail, shows that Occidental Petroleum had debt of US$36.9b at the end of March 2021, a reduction from US$40.2b over a year. However, it does have US$2.27b in cash offsetting this, leading to net debt of about US$34.7b.

A Look At Occidental Petroleum’s Liabilities

The latest balance sheet data shows that Occidental Petroleum had liabilities of US$8.63b due within a year, and liabilities of US$52.4b falling due after that. Offsetting these obligations, it had cash of US$2.27b as well as receivables valued at US$3.05b due within 12 months. So it has liabilities totalling US$55.7b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$23.4b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Occidental Petroleum would probably need a major re-capitalization if its creditors were to demand repayment. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Occidental Petroleum can strengthen its balance sheet over time.

In the last year Occidental Petroleum had a loss before interest and tax, and actually shrunk its revenue by 30%, to US$16b. To be frank that doesn’t bode well.

Caveat Emptor

While Occidental Petroleum’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping US$8.7b. Considering that alongside the liabilities mentioned above make us nervous about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. For example, we would not want to see a repeat of last year’s loss of US$12b. And until that time we think this is a risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.