Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, NVIDIA Corporation (NASDAQ:NVDA) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does NVIDIA Carry?

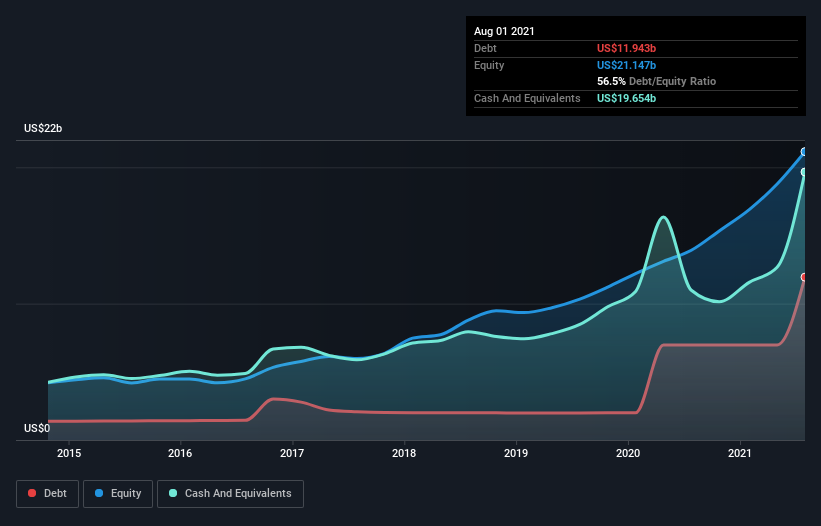

You can click the graphic below for the historical numbers, but it shows that as of August 2021 NVIDIA had US$11.9b of debt, an increase on US$6.96b, over one year. But on the other hand it also has US$19.7b in cash, leading to a US$7.71b net cash position.

How Healthy Is NVIDIA’s Balance Sheet?

According to the last reported balance sheet, NVIDIA had liabilities of US$4.45b due within 12 months, and liabilities of US$13.1b due beyond 12 months. On the other hand, it had cash of US$19.7b and US$3.59b worth of receivables due within a year. So it actually has US$5.74b more liquid assets than total liabilities.

Having regard to NVIDIA’s size, it seems that its liquid assets are well balanced with its total liabilities. So while it’s hard to imagine that the US$561.1b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Succinctly put, NVIDIA boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that NVIDIA has boosted its EBIT by 96%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine NVIDIA’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. NVIDIA may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, NVIDIA actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that NVIDIA has net cash of US$7.71b, as well as more liquid assets than liabilities. The cherry on top was that in converted 106% of that EBIT to free cash flow, bringing in US$6.7b. So is NVIDIA’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.