Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Nova Ltd. (NASDAQ:NVMI) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Nova’s Debt?

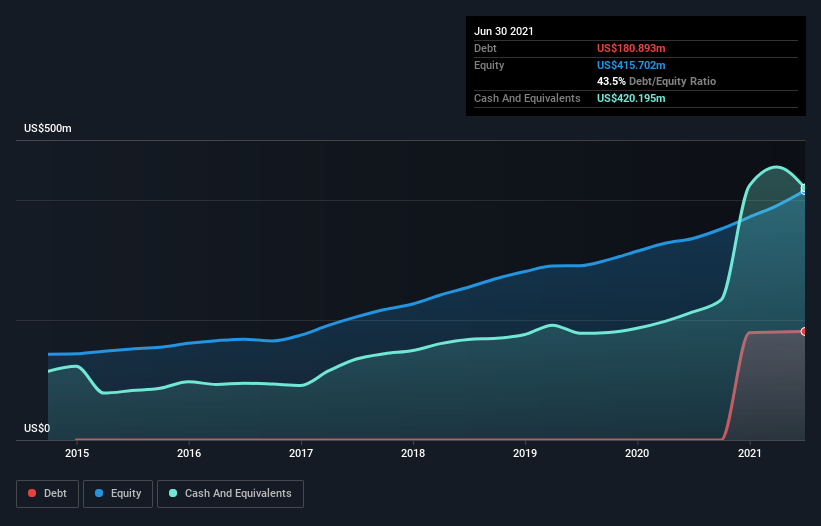

The image below, which you can click on for greater detail, shows that at June 2021 Nova had debt of US$180.9m, up from none in one year. However, it does have US$420.2m in cash offsetting this, leading to net cash of US$239.3m.

How Strong Is Nova’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Nova had liabilities of US$257.0m due within 12 months and liabilities of US$44.4m due beyond that. Offsetting this, it had US$420.2m in cash and US$58.2m in receivables that were due within 12 months. So it actually has US$176.9m more liquid assets than total liabilities.

This surplus suggests that Nova has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Nova boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that Nova has boosted its EBIT by 68%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Nova can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Nova has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Nova recorded free cash flow worth a fulsome 84% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Summing up

While it is always sensible to investigate a company’s debt, in this case Nova has US$239.3m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 84% of that EBIT to free cash flow, bringing in US$82m. So is Nova’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet.