Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Nordstrom, Inc. (NYSE:JWN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Nordstrom Carry?

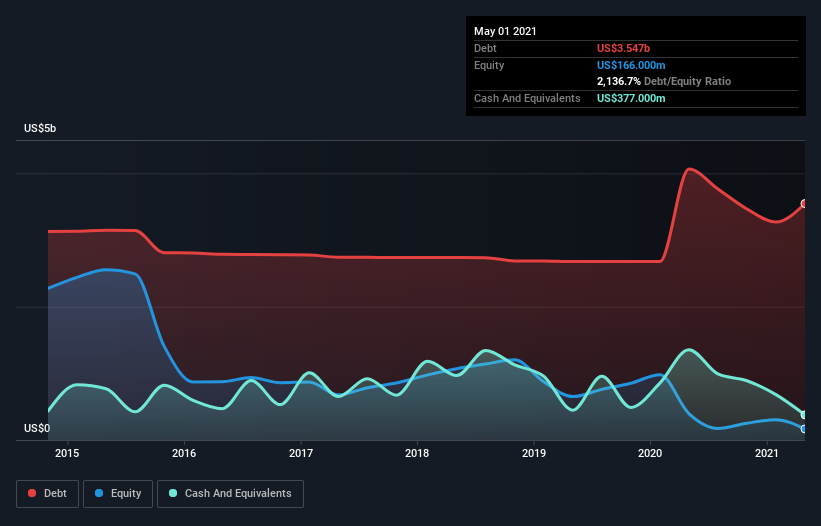

The image below, which you can click on for greater detail, shows that Nordstrom had debt of US$3.55b at the end of May 2021, a reduction from US$4.06b over a year. However, it also had US$377.0m in cash, and so its net debt is US$3.17b.

A Look At Nordstrom’s Liabilities

The latest balance sheet data shows that Nordstrom had liabilities of US$4.01b due within a year, and liabilities of US$5.16b falling due after that. Offsetting this, it had US$377.0m in cash and US$814.0m in receivables that were due within 12 months. So it has liabilities totalling US$7.98b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company’s market capitalization of US$5.72b, we think shareholders really should watch Nordstrom’s debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Nordstrom can strengthen its balance sheet over time.

Over 12 months, Nordstrom made a loss at the EBIT level, and saw its revenue drop to US$12b, which is a fall of 18%. That’s not what we would hope to see.

Caveat Emptor

Not only did Nordstrom’s revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost US$432m at the EBIT level. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through US$314m in negative free cash flow over the last year. That means it’s on the risky side of things. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.