Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Netflix, Inc. (NASDAQ:NFLX) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Netflix Carry?

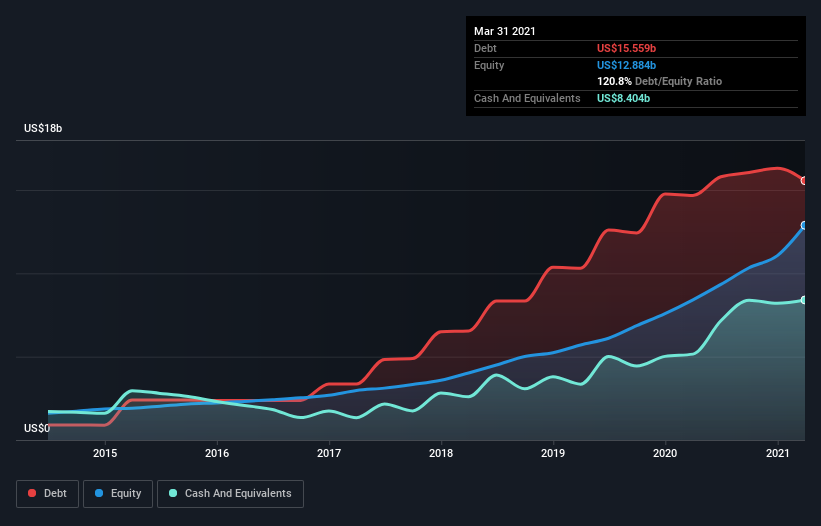

As you can see below, at the end of March 2021, Netflix had US$15.6b of debt, up from US$14.7b a year ago. Click the image for more detail. However, because it has a cash reserve of US$8.40b, its net debt is less, at about US$7.16b.

How Strong Is Netflix’s Balance Sheet?

We can see from the most recent balance sheet that Netflix had liabilities of US$7.96b falling due within a year, and liabilities of US$19.3b due beyond that. Offsetting this, it had US$8.40b in cash and US$807.0m in receivables that were due within 12 months. So its liabilities total US$18.0b more than the combination of its cash and short-term receivables.

Given Netflix has a humongous market capitalization of US$236.3b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Netflix has net debt of just 1.3 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 7.6 times, which is more than adequate. In addition to that, we’re happy to report that Netflix has boosted its EBIT by 80%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Netflix can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Netflix saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Netflix’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its EBIT growth rate. When we consider all the elements mentioned above, it seems to us that Netflix is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. The balance sheet is clearly the area to focus on when you are analysing debt.