The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Middlesex Water Company (NASDAQ:MSEX) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Middlesex Water’s Debt?

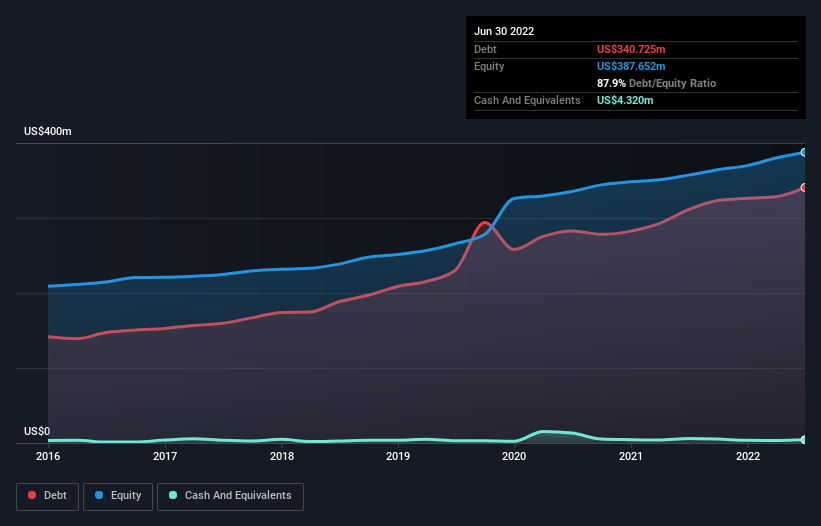

The image below, which you can click on for greater detail, shows that at June 2022 Middlesex Water had debt of US$340.7m, up from US$311.2m in one year. And it doesn’t have much cash, so its net debt is about the same.

How Strong Is Middlesex Water’s Balance Sheet?

We can see from the most recent balance sheet that Middlesex Water had liabilities of US$78.8m falling due within a year, and liabilities of US$571.5m due beyond that. On the other hand, it had cash of US$4.32m and US$24.9m worth of receivables due within a year. So it has liabilities totalling US$621.1m more than its cash and near-term receivables, combined.

Middlesex Water has a market capitalization of US$1.43b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With a net debt to EBITDA ratio of 5.1, it’s fair to say Middlesex Water does have a significant amount of debt. However, its interest coverage of 4.5 is reasonably strong, which is a good sign. Notably Middlesex Water’s EBIT was pretty flat over the last year. Ideally it can diminish its debt load by kick-starting earnings growth. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Middlesex Water’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Middlesex Water burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Middlesex Water’s net debt to EBITDA left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But at least its EBIT growth rate is not so bad. We should also note that Water Utilities industry companies like Middlesex Water commonly do use debt without problems. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Middlesex Water stock a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt.