The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Lions Gate Entertainment Corp. (NYSE:LGF.A) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Lions Gate Entertainment’s Debt?

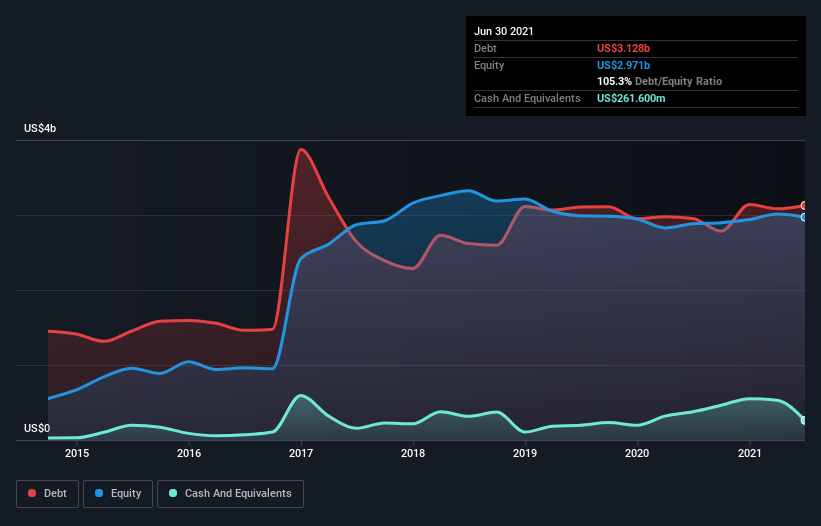

The image below, which you can click on for greater detail, shows that at June 2021 Lions Gate Entertainment had debt of US$3.13b, up from US$2.95b in one year. However, it does have US$261.6m in cash offsetting this, leading to net debt of about US$2.87b.

How Strong Is Lions Gate Entertainment’s Balance Sheet?

The latest balance sheet data shows that Lions Gate Entertainment had liabilities of US$1.56b due within a year, and liabilities of US$3.69b falling due after that. Offsetting these obligations, it had cash of US$261.6m as well as receivables valued at US$502.8m due within 12 months. So it has liabilities totalling US$4.48b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$2.84b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Lions Gate Entertainment would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Lions Gate Entertainment shareholders face the double whammy of a high net debt to EBITDA ratio (7.2), and fairly weak interest coverage, since EBIT is just 0.79 times the interest expense. The debt burden here is substantial. Worse, Lions Gate Entertainment’s EBIT was down 49% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Lions Gate Entertainment can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Lions Gate Entertainment produced sturdy free cash flow equating to 76% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

On the face of it, Lions Gate Entertainment’s interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Taking into account all the aforementioned factors, it looks like Lions Gate Entertainment has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. There’s no doubt that we learn most about debt from the balance sheet.