Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Lamb Weston Holdings, Inc. (NYSE:LW) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Lamb Weston Holdings Carry?

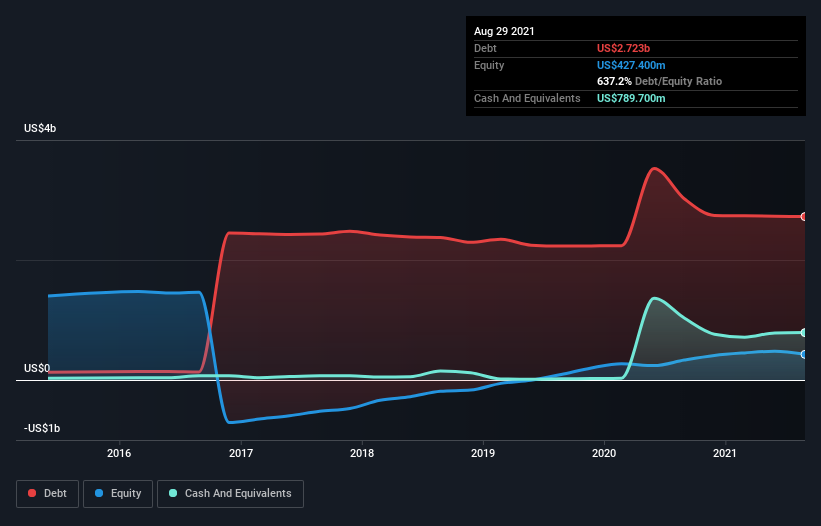

As you can see below, Lamb Weston Holdings had US$2.72b of debt at August 2021, down from US$3.02b a year prior. However, because it has a cash reserve of US$789.7m, its net debt is less, at about US$1.93b.

How Strong Is Lamb Weston Holdings’ Balance Sheet?

We can see from the most recent balance sheet that Lamb Weston Holdings had liabilities of US$650.0m falling due within a year, and liabilities of US$3.10b due beyond that. On the other hand, it had cash of US$789.7m and US$401.3m worth of receivables due within a year. So it has liabilities totalling US$2.56b more than its cash and near-term receivables, combined.

Lamb Weston Holdings has a market capitalization of US$8.18b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Lamb Weston Holdings’s debt is 3.3 times its EBITDA, and its EBIT cover its interest expense 3.5 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Even worse, Lamb Weston Holdings saw its EBIT tank 23% over the last 12 months. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Lamb Weston Holdings’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Lamb Weston Holdings recorded free cash flow worth 68% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Lamb Weston Holdings’s struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. In particular, its conversion of EBIT to free cash flow was re-invigorating. When we consider all the factors discussed, it seems to us that Lamb Weston Holdings is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt.