The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies KVH Industries, Inc. (NASDAQ:KVHI) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is KVH Industries’s Debt?

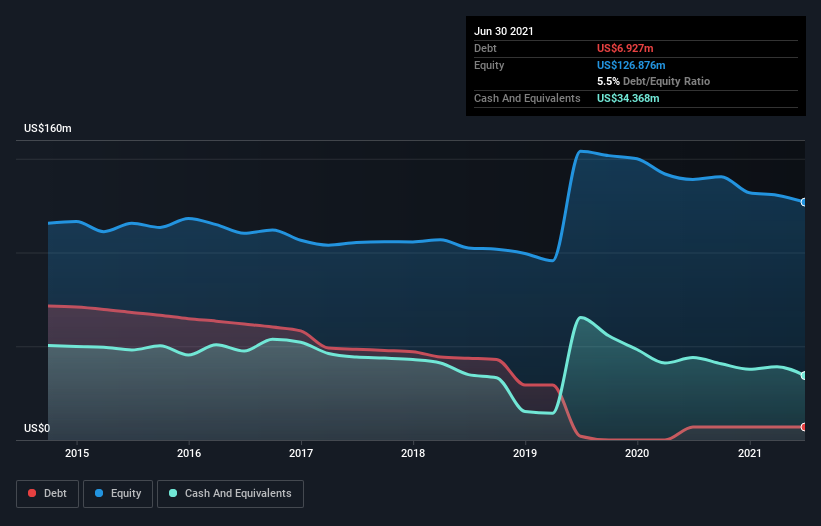

The chart below, which you can click on for greater detail, shows that KVH Industries had US$6.93m in debt in June 2021; about the same as the year before. But it also has US$34.4m in cash to offset that, meaning it has US$27.4m net cash.

How Healthy Is KVH Industries’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that KVH Industries had liabilities of US$42.7m due within 12 months and liabilities of US$6.98m due beyond that. Offsetting this, it had US$34.4m in cash and US$34.1m in receivables that were due within 12 months. So it actually has US$18.8m more liquid assets than total liabilities.

This surplus suggests that KVH Industries has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that KVH Industries has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine KVH Industries’s ability to maintain a healthy balance sheet going forward.

In the last year KVH Industries wasn’t profitable at an EBIT level, but managed to grow its revenue by 10%, to US$171m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is KVH Industries?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that KVH Industries had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$13m and booked a US$22m accounting loss. However, it has net cash of US$27.4m, so it has a bit of time before it will need more capital. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly. When analysing debt levels, the balance sheet is the obvious place to start.