Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Kohl’s Corporation (NYSE:KSS) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

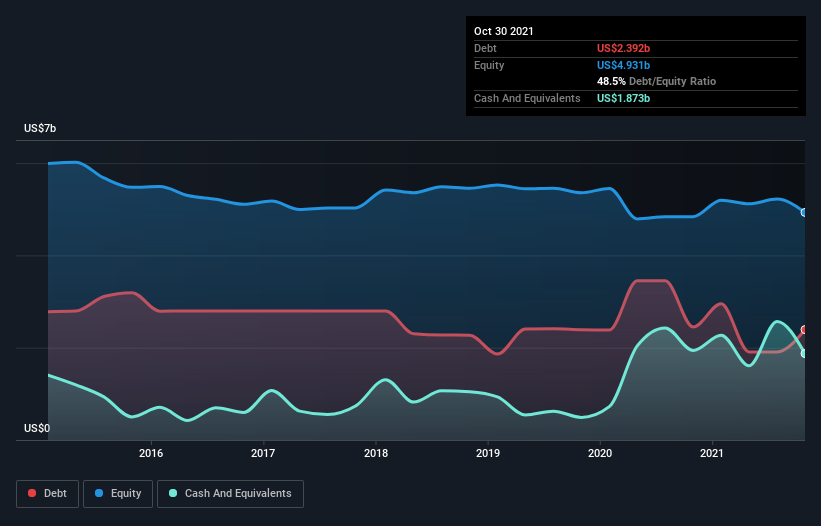

What Is Kohl’s’s Net Debt?

The chart below, which you can click on for greater detail, shows that Kohl’s had US$2.39b in debt in October 2021; about the same as the year before. However, because it has a cash reserve of US$1.87b, its net debt is less, at about US$519.0m.

How Healthy Is Kohl’s’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kohl’s had liabilities of US$3.94b due within 12 months and liabilities of US$7.08b due beyond that. On the other hand, it had cash of US$1.87b and US$789.0m worth of receivables due within a year. So it has liabilities totalling US$8.36b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company’s market capitalization of US$6.52b, we think shareholders really should watch Kohl’s’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 0.19 times EBITDA, Kohl’s is arguably pretty conservatively geared. And it boasts interest cover of 7.0 times, which is more than adequate. It was also good to see that despite losing money on the EBIT line last year, Kohl’s turned things around in the last 12 months, delivering and EBIT of US$1.9b. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Kohl’s can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Kohl’s recorded free cash flow worth a fulsome 91% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

Both Kohl’s’s ability to to convert EBIT to free cash flow and its net debt to EBITDA gave us comfort that it can handle its debt. In contrast, our confidence was undermined by its apparent struggle to handle its total liabilities. Looking at all this data makes us feel a little cautious about Kohl’s’s debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. There’s no doubt that we learn most about debt from the balance sheet.