Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Kala Pharmaceuticals, Inc. (NASDAQ:KALA) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Kala Pharmaceuticals’s Net Debt?

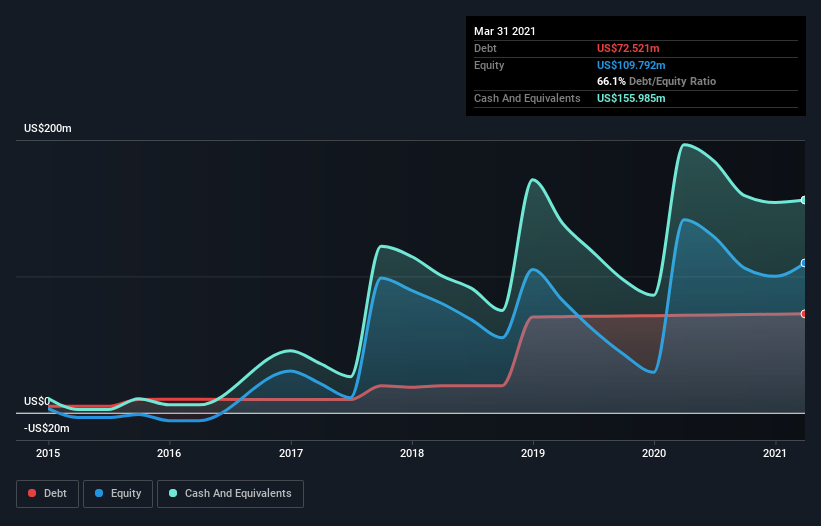

As you can see below, Kala Pharmaceuticals had US$72.5m of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$156.0m in cash, so it actually has US$83.5m net cash.

A Look At Kala Pharmaceuticals’ Liabilities

We can see from the most recent balance sheet that Kala Pharmaceuticals had liabilities of US$20.0m falling due within a year, and liabilities of US$100.0m due beyond that. Offsetting this, it had US$156.0m in cash and US$12.2m in receivables that were due within 12 months. So it actually has US$48.2m more liquid assets than total liabilities.

It’s good to see that Kala Pharmaceuticals has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Kala Pharmaceuticals has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Kala Pharmaceuticals’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Kala Pharmaceuticals reported revenue of US$8.6m, which is a gain of 49%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Kala Pharmaceuticals?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Kala Pharmaceuticals lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$105m and booked a US$113m accounting loss. However, it has net cash of US$83.5m, so it has a bit of time before it will need more capital. Kala Pharmaceuticals’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt.