Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that International Paper Company (NYSE:IP) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does International Paper Carry?

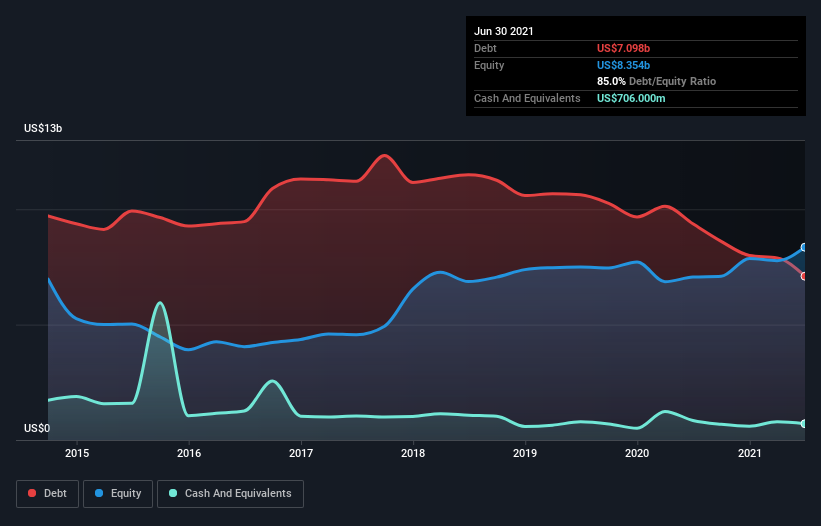

You can click the graphic below for the historical numbers, but it shows that International Paper had US$7.10b of debt in June 2021, down from US$9.37b, one year before. On the flip side, it has US$706.0m in cash leading to net debt of about US$6.39b.

How Healthy Is International Paper’s Balance Sheet?

The latest balance sheet data shows that International Paper had liabilities of US$8.64b due within a year, and liabilities of US$14.5b falling due after that. Offsetting this, it had US$706.0m in cash and US$4.02b in receivables that were due within 12 months. So its liabilities total US$18.4b more than the combination of its cash and short-term receivables.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$22.3b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

International Paper has net debt worth 2.1 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.2 times the interest expense. While these numbers do not alarm us, it’s worth noting that the cost of the company’s debt is having a real impact. Unfortunately, International Paper saw its EBIT slide 9.3% in the last twelve months. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if International Paper can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, International Paper actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Neither International Paper’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. We think that International Paper’s debt does make it a bit risky, after considering the aforementioned data points together. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.