David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Hasbro, Inc. (NASDAQ:HAS) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Hasbro’s Debt?

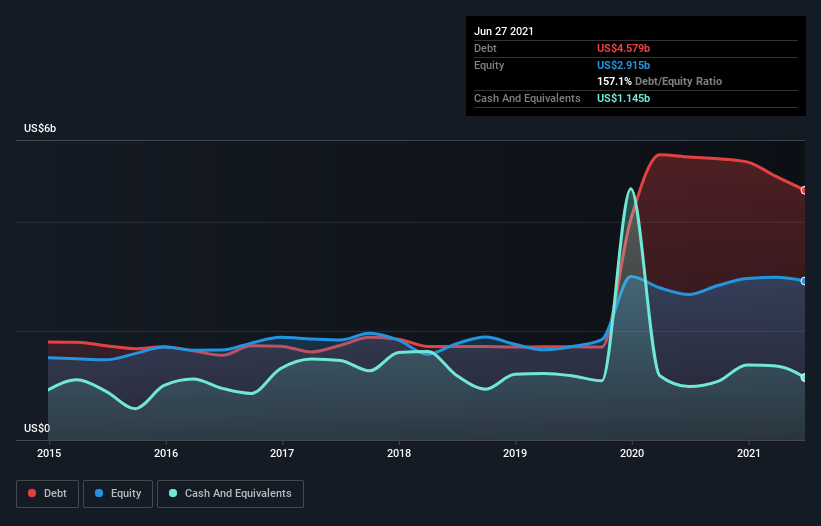

As you can see below, Hasbro had US$4.58b of debt at June 2021, down from US$5.19b a year prior. On the flip side, it has US$1.15b in cash leading to net debt of about US$3.43b.

How Strong Is Hasbro’s Balance Sheet?

We can see from the most recent balance sheet that Hasbro had liabilities of US$2.05b falling due within a year, and liabilities of US$5.14b due beyond that. On the other hand, it had cash of US$1.15b and US$1.12b worth of receivables due within a year. So it has liabilities totalling US$4.92b more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Hasbro is worth a massive US$12.7b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hasbro’s debt is 2.9 times its EBITDA, and its EBIT cover its interest expense 4.9 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Importantly, Hasbro grew its EBIT by 44% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Hasbro can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Hasbro recorded free cash flow worth a fulsome 91% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Hasbro’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. When we consider the range of factors above, it looks like Hasbro is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. B