The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, IDEXX Laboratories, Inc. (NASDAQ:IDXX) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is IDEXX Laboratories’s Net Debt?

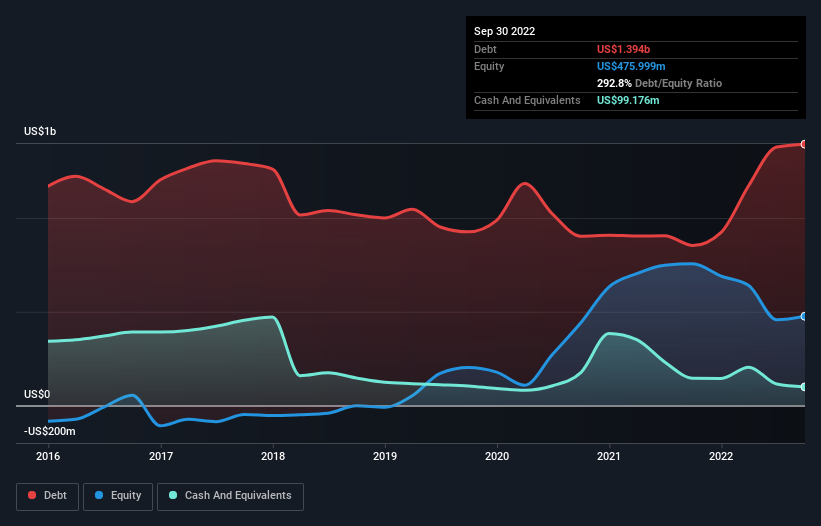

As you can see below, at the end of September 2022, IDEXX Laboratories had US$1.39b of debt, up from US$853.0m a year ago. Click the image for more detail. However, because it has a cash reserve of US$99.2m, its net debt is less, at about US$1.29b.

How Strong Is IDEXX Laboratories’ Balance Sheet?

We can see from the most recent balance sheet that IDEXX Laboratories had liabilities of US$1.19b falling due within a year, and liabilities of US$974.1m due beyond that. Offsetting these obligations, it had cash of US$99.2m as well as receivables valued at US$452.9m due within 12 months. So its liabilities total US$1.61b more than the combination of its cash and short-term receivables.

Of course, IDEXX Laboratories has a titanic market capitalization of US$34.5b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

IDEXX Laboratories has a low net debt to EBITDA ratio of only 1.3. And its EBIT covers its interest expense a whopping 26.6 times over. So we’re pretty relaxed about its super-conservative use of debt. But the other side of the story is that IDEXX Laboratories saw its EBIT decline by 5.1% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine IDEXX Laboratories’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, IDEXX Laboratories recorded free cash flow worth 64% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that IDEXX Laboratories’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its EBIT growth rate does undermine this impression a bit. We would also note that Medical Equipment industry companies like IDEXX Laboratories commonly do use debt without problems. Taking all this data into account, it seems to us that IDEXX Laboratories takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. When analysing debt levels, the balance sheet is the obvious place to start.