David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Hubbell Incorporated (NYSE:HUBB) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Hubbell’s Net Debt?

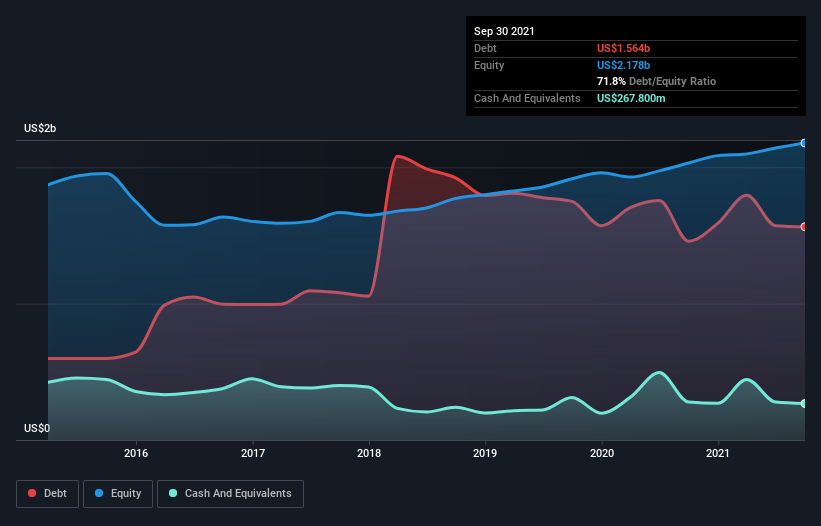

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Hubbell had US$1.56b of debt, an increase on US$1.46b, over one year. However, it does have US$267.8m in cash offsetting this, leading to net debt of about US$1.30b.

How Strong Is Hubbell’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hubbell had liabilities of US$1.04b due within 12 months and liabilities of US$2.03b due beyond that. Offsetting these obligations, it had cash of US$267.8m as well as receivables valued at US$798.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.00b.

Hubbell has a market capitalization of US$9.95b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hubbell’s net debt to EBITDA ratio of about 1.8 suggests only moderate use of debt. And its strong interest cover of 10.1 times, makes us even more comfortable. Sadly, Hubbell’s EBIT actually dropped 3.1% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Hubbell can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Hubbell generated free cash flow amounting to a very robust 83% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Hubbell’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But truth be told we feel its EBIT growth rate does undermine this impression a bit. All these things considered, it appears that Hubbell can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one.