Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Hub Group, Inc. (NASDAQ:HUBG) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Hub Group’s Debt?

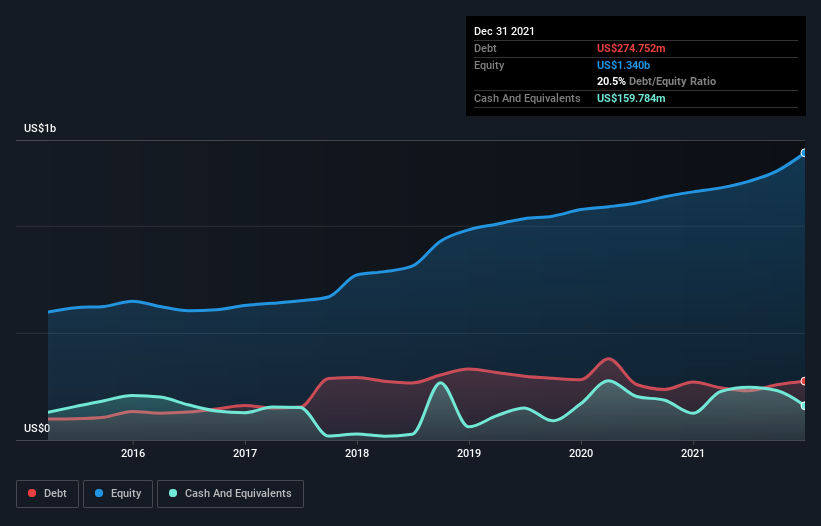

The chart below, which you can click on for greater detail, shows that Hub Group had US$274.8m in debt in December 2021; about the same as the year before. On the flip side, it has US$159.8m in cash leading to net debt of about US$115.0m.

How Strong Is Hub Group’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hub Group had liabilities of US$687.1m due within 12 months and liabilities of US$409.9m due beyond that. Offsetting this, it had US$159.8m in cash and US$704.5m in receivables that were due within 12 months. So its liabilities total US$232.7m more than the combination of its cash and short-term receivables.

Of course, Hub Group has a market capitalization of US$2.71b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hub Group has a low net debt to EBITDA ratio of only 0.31. And its EBIT easily covers its interest expense, being 32.7 times the size. So we’re pretty relaxed about its super-conservative use of debt. Even more impressive was the fact that Hub Group grew its EBIT by 110% over twelve months. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Hub Group’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Hub Group recorded free cash flow worth 67% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Hub Group’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Overall, we don’t think Hub Group is taking any bad risks, as its debt load seems modest. So we’re not worried about the use of a little leverage on the balance sheet.