Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies The Hershey Company (NYSE:HSY) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

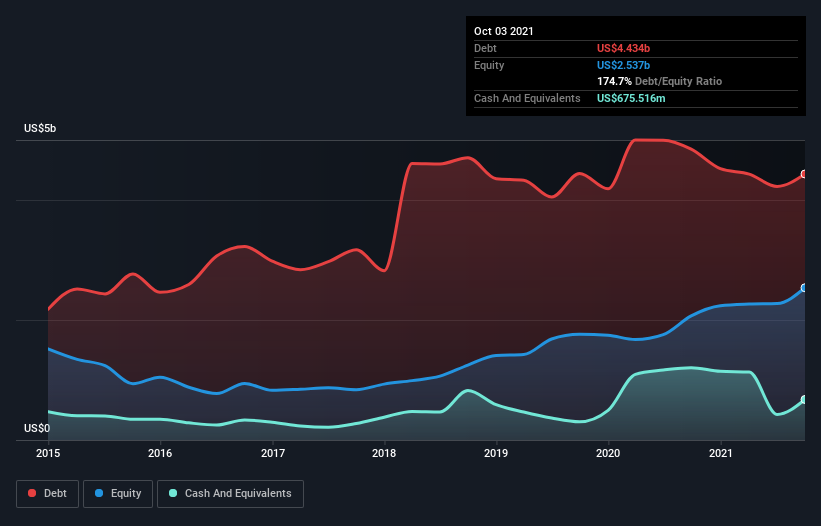

What Is Hershey’s Net Debt?

As you can see below, Hershey had US$4.43b of debt at October 2021, down from US$4.85b a year prior. However, it does have US$675.5m in cash offsetting this, leading to net debt of about US$3.76b.

A Look At Hershey’s Liabilities

We can see from the most recent balance sheet that Hershey had liabilities of US$1.91b falling due within a year, and liabilities of US$5.00b due beyond that. Offsetting this, it had US$675.5m in cash and US$841.2m in receivables that were due within 12 months. So it has liabilities totalling US$5.39b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Hershey has a huge market capitalization of US$26.6b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hershey’s net debt to EBITDA ratio of about 1.6 suggests only moderate use of debt. And its strong interest cover of 14.9 times, makes us even more comfortable. Also good is that Hershey grew its EBIT at 15% over the last year, further increasing its ability to manage debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hershey can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Hershey recorded free cash flow worth 79% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Hershey’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Zooming out, Hershey seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. The balance sheet is clearly the area to focus on when you are analysing debt.